The insurance coverage gap: 40% of homeowners are opting out of additional protection

Your homeowners insurance can help protect your home and finances, but do you know if your policy covers storm surge flooding? What about an overflowing sump pump? Most standard home insurance plans don't. When your base policy isn’t enough, that's where insurance riders come in. Insurance riders, also known as endorsements or add-ons, can cover damage a base policy doesn't, like damaged valuables, floods, or earthquakes.

But Hippo’s 2026 Housepower Report shows that nearly half of homeowners don't have insurance riders. What's more, some may not realize that their base insurance policy doesn't offer protection for many of these potentially expensive events. Our data reveals why homeowners get additional insurance, and, perhaps more importantly, why they don't.

Key takeaways

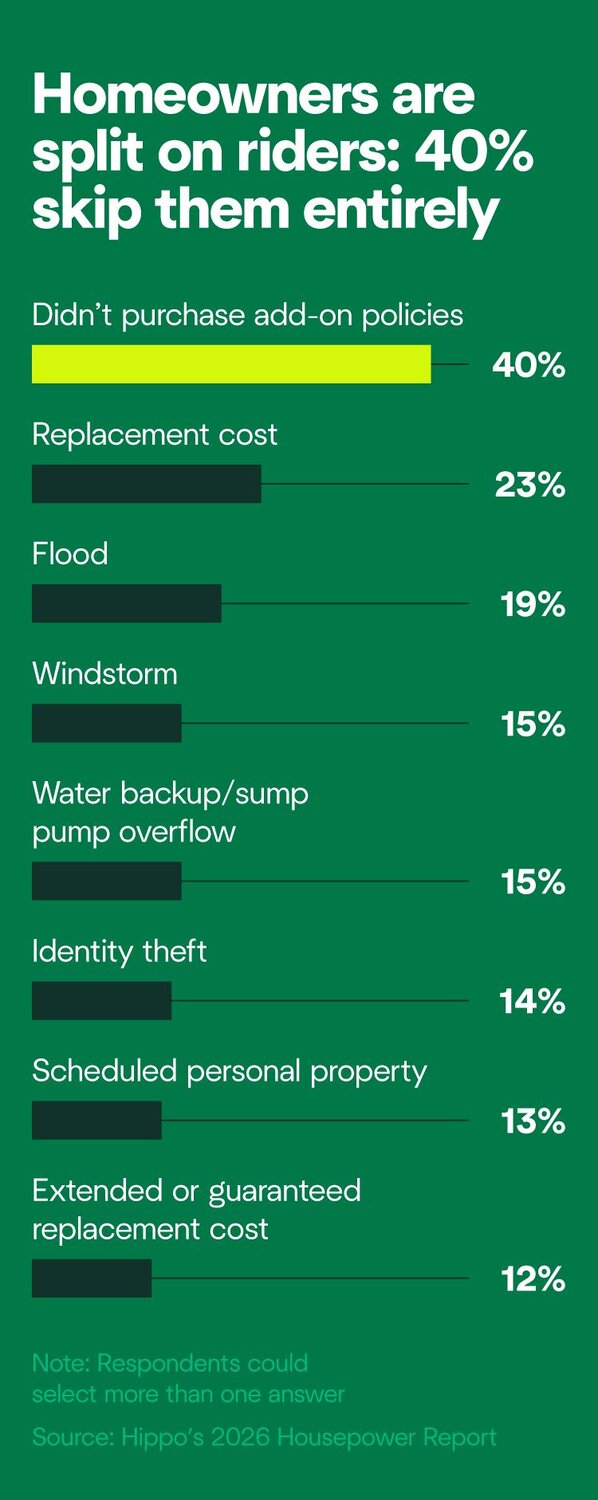

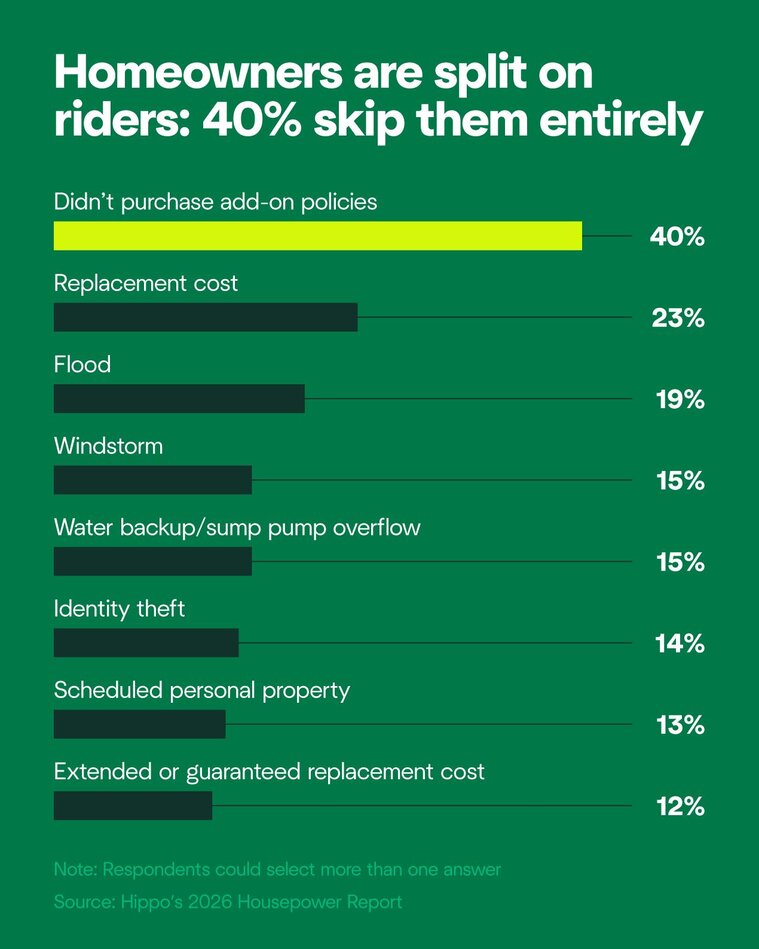

- 40% of homeowners don't have insurance riders (also known as add-on policies).

- 23% of homeowners have purchased replacement cost riders for their home insurance. It's the most popular kind of insurance rider, followed by flood (19%), windstorm (15%), and water backup or sump pump overflow (15%).

- 70% of homeowners in Alaska, California, Hawaii, Oregon, and Washington have insurance riders, the highest percentage of any U.S. region. Wildfires and other extreme weather in that area may incentivize homeowners to sign up for extra coverage.

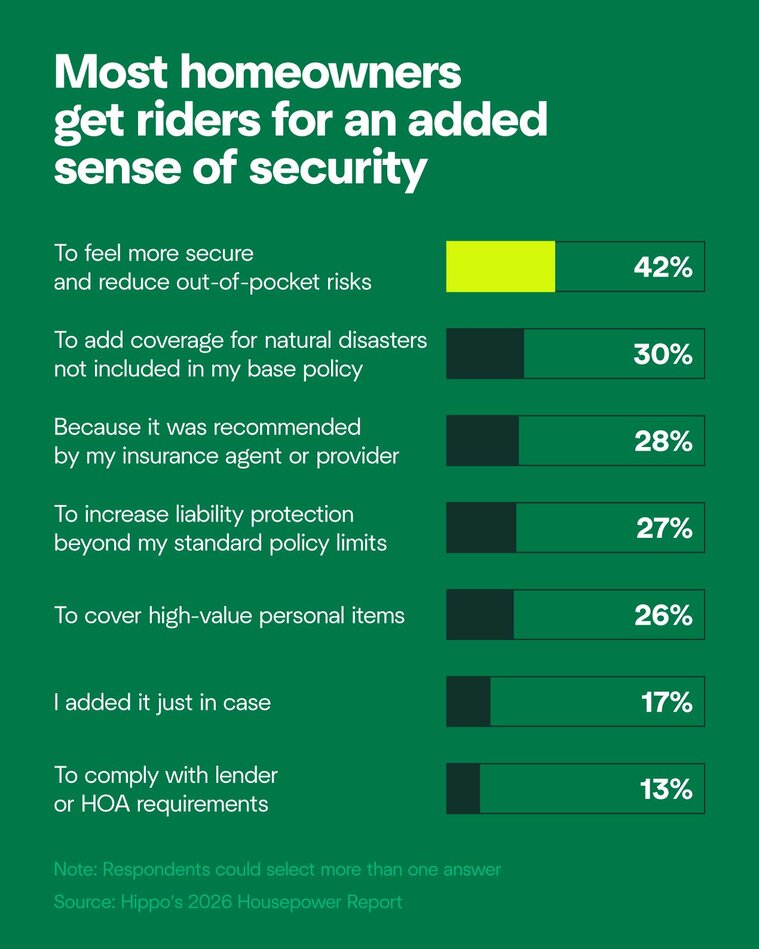

- 42% of homeowners purchased an insurance rider to feel more secure and reduce out-of-pocket risks, which was the most common reason.

Many homeowners pick insurance riders for a sense of added security

Most homeowners with a mortgage will be required to carry homeowners insurance, but 40% of U.S. homeowners don't have riders. Insurance riders are often optional, but depending on a person's type of home and where they live, skipping additional coverage could leave gaps in protection.

For example, take scheduled personal property riders, which cover specific, high-value items, such as jewelry or electronics. An individual's insurance may not cover the full value of these pieces.

On average, people lose $2,661 in items during a burglary,1 but replacement riders typically cost only $1 to $2 per $100 of value. Covering $2,661 in valuables may cost around $26 to $53 annually. While it's an additional cost, it could save many homeowners significantly if they ever need to replace stolen or lost valuables.

Most people signed up for insurance riders for the same reason they would purchase any other type of insurance—for a sense of safety. Around 2 in 5 (42%) homeowners purchased an insurance rider to feel more secure and reduce the risk of out-of-pocket costs.

Homeowners Are Split on Riders: 40% Skip Them Entirely

While riders are generally optional, 40% of homeowners elect not to purchase them and stick with their base policy.

The homeowners that select riders often opt for broad coverage for unspecified damage. Most commonly, 23% of homeowners have replacement cost riders. This add-on covers repair or replacement costs for damaged property, and doesn't deduct for depreciation. In other words, you'll receive the value of your property as if it were brand new.

About 1 in 10 (12%) homeowners have extended cost or guaranteed replacement cost riders, which are two different ways to cover repairs if costs suddenly spike due to local demand or shortages. This is often useful after disasters that cause widespread damage, like hurricanes, tornadoes, or wildfires. Extended cost riders raise your dwelling coverage limit by about 10% to 50%, while guaranteed replacement riders cover your entire home in a total loss, even if the value exceeds your policy limit.

Other relatively common riders are more specific. They include flood (19%), windstorm (15%), and water backup or sump pump overflow (15%).

80% of homeowners think their insurance covers storms. Most haven't checked.

We learned in a past survey on extreme weather that 80% of homeowners are confident they have adequate coverage for severe weather or storm damage, but only 32% reviewed their insurance in the past year to understand their weather-related coverage. As climate change leads to more frequent and severe storms, knowing your insurance terms is more important than ever.

From Google to AI, there are more tools than ever to research insurance options. Whatever tools you use to research your options, speaking with a licensed insurance agent before making any major decisions is always a good idea.

For example, flooding is increasingly common across the country, but unlike a burst pipe, flooding caused by extreme weather is rarely covered by homeowners' insurance. With that in mind, 30% of homeowners purchased an insurance rider to add coverage for natural disasters not included in their base policy.

Not every U.S. region experiences the same extreme weather, so location impacts the likelihood that someone has riders. More than two-thirds (70%) of people in the Pacific states of Alaska, California, Hawaii, Oregon, and Washington have insurance riders, the highest percentage of any region.

Because of climate change, the western U.S. is becoming hotter and drier, increasing the region's risk of devastating wildfires and drought, which may not be covered by a person's base insurance.2 So it makes sense that 37% of West Coast residents say they added coverage for natural disasters not included in their base insurance.

On the other hand, around a third (32%) of homeowners nationwide who don't feel prepared for severe weather have riders to feel secure. Purchasing catastrophe home insurance doesn't guarantee you're more prepared for potential fire, earthquakes, or flooding, but if you live in an area prone to severe weather, it may be important to consider it.

Nearly 1 in 3 homeowners without riders don't think they need extra coverage, but that may not be true

So, what keeps people from purchasing a rider? Around one-third (32%) of homeowners say their current homeowners policy provides sufficient coverage, so they didn't purchase the riders they considered. Also, 23% say the cost of add-on policies is too high for them, and 22% say the risk in their area doesn't justify the cost.

Home insurance riders can sometimes cost as little as a few dollars per month, but the price can climb to several thousand dollars a year for risks like owning extremely valuable personal items or living in high-risk weather zones. Under the National Flood Insurance Program's rates, the median cost of a single-family home's insurance policy in the U.S. is $786 per year. But insurance for homes in areas more susceptible to flooding costs a median of $1,290, a 49% increase.3

Accordingly, 28% of homeowners not prepared for severe weather say they didn't purchase riders they had considered because the cost was too high, the most common reason for that group. Around 1 in 5 (22%) of those homeowners say they believe their current homeowners' policy provides sufficient coverage.

This, too, varies based on where homeowners live. Most commonly, 21% of people in the South Atlantic region (East Coast states from Delaware to Florida) don't have insurance riders, followed by 17% in the East North Central region, which includes the Midwest states of Illinois, Indiana, Michigan, Ohio, and Wisconsin.

Many homeowners in those Midwest states may be foregoing riders because they're at relatively low risk of climate change-related disasters. Others may be unable to afford it. In Florida, for instance, insurance for homes in riskier areas costs 55% more than standard home insurance.3

All in all, nearly 1 in 5 (18%) homeowners considered purchasing replacement cost riders for their home insurance for 2026, but decided against it. A similar percentage (13%) considered an extended replacement cost rider.

Beyond the obvious benefit of covering your home in case of an emergency, extra coverage can offer long-term benefits and immediate peace of mind. Consider the future when deciding whether to accept riders or not.

What to know before choosing a homeowners insurance rider

Do you need to add riders to your homeowners' insurance policy? We can't answer that for you, but we can recommend a few things to consider before you make a decision:

Your risk factors

If you don't own any expensive valuables or aren't concerned about water backup or service line damage, you may not need to consider those riders. Weather-related riders are trickier, because people often don't realize that homeowners' insurance doesn’t cover earthquakes or floods. They may not even be aware that their home is at risk of weather damage at all.

To learn if your home could be vulnerable to earthquakes or floods, go to the federal government's record of earthquakes across the country and check your address against the Federal Emergency Management Agency's (FEMA) flood map. Many insurance providers offer flood, earthquake, and hurricane riders to protect your home against damage or total loss.

You could also consider catastrophe insurance, a separate insurance policy that typically covers a variety of weather-related damage, depending on the policy.

However, keep in mind that if your home is at very high risk of flooding, wildfires, or other disasters, some insurance providers may not cover it at all. Some states, like California, have government-backed insurance plans for those homeowners.4 Check with your state to see if it offers a similar program.

Your budget priorities

Insurance riders are an extra cost on top of your homeowners insurance policy, but they're priced differently depending on the rider. Riders for jewelry and collectible items might cost $1 to $2 annually per $100 of value, and extended replacement cost coverage might cost $25 to $75 annually. Weather-related riders can cost more.

Your risk tolerance

Generally, if your home is at risk of weather, crime, or other factors, insurance riders can be a long-term investment over time that can help protect you from having to repair major damage completely out of pocket.

Consider your budget and your coverage needs when reviewing your homeowners policy. Don't be afraid to ask plenty of questions about what a rider would cover, its deductible (if it has one), and any other terms.

If you're just beginning your search, Hippo can be your partner in finding insurance quotes for your unique home. Check out our Learn Center to find out more about unfamiliar insurance terms and use our search to find affordable rates near you.

Methodology

Any data referencing the 2026 Housepower Survey was collected on September 22, 2025, and conducted by Centiment on behalf of Hippo Insurance Services. The results are based on 1,619 completed surveys. In order to qualify, respondents were screened to be residents of the United States, over 18 years of age, and homeowners. Data is census-balanced, and the margin of error is approximately ±2% for the overall sample with a 95% confidence level.

The MOE and confidence level for data filtered by specific demographics (subgroups) may differ from the overall result. Because these subgroups are naturally smaller than the total sample, they may have a larger margin of error than the ±2% for the full data set.

External sources

- U.S. Federal Bureau of Investigation. (2019) 2019 Crime in the United States

- National Oceanic and Atmospheric Administration. (2023) Wildfire climate connection

- Federal Emergency Management Agency. (2023) Cost of Flood Insurance for Single-Family Homes under NFIP’s Pricing Approach

- California Department of Insurance. California FAIR Plan

This article is for informational purposes only. The content reflects general homeowner considerations and is not professional advice. It also includes observed trends within the surveyed population and certain additional information compiled from sources not affiliated with Hippo. While we believe this information to be reliable, we do not guarantee its accuracy or completeness. For any insurance-related decision, please consult your licensed insurance producer.

Sources cited are publicly available and referenced in April 2026.

Related articles

AI adoption study: The growing generational divide in home insurance

Homeowner's Guide to Extreme Weather in 2026: What's Next and How To Prepare

Confronting Home Repair Scams: Experts Weigh In on How To Protect Yourself

Hippo Resilience Report: Best States for Climate Change

5-year housing forecast: Why almost 1 in 3 homeowners are planning their exit