Severe Weather Prep Report: How Homeowners Are Bracing for Costs

2024 is no stranger to extreme weather. In the past few months, California declared a state of emergency in response to life-threatening severe storms (Office of Governor Gavin Newsom February 2024); Winter Storm Finn brought blizzard conditions throughout the Plains, Rockies, and Midwest (The Weather Channel); and Winter Storm Heather brought heavy snow and icy conditions from the Northwest to the South (The Weather Channel).

Heavy rain, snow, and wind can take a toll on homes. Now is the time for homeowners to prioritize preventative measures to help them stay ahead of major problems.

We surveyed U.S.-based homeowners to learn about how confident they are with their insurance coverage, external factors impacting their financial preparations for severe weather, and what preparations they have been able to take so far.

Key takeaways from responding homeowners

-

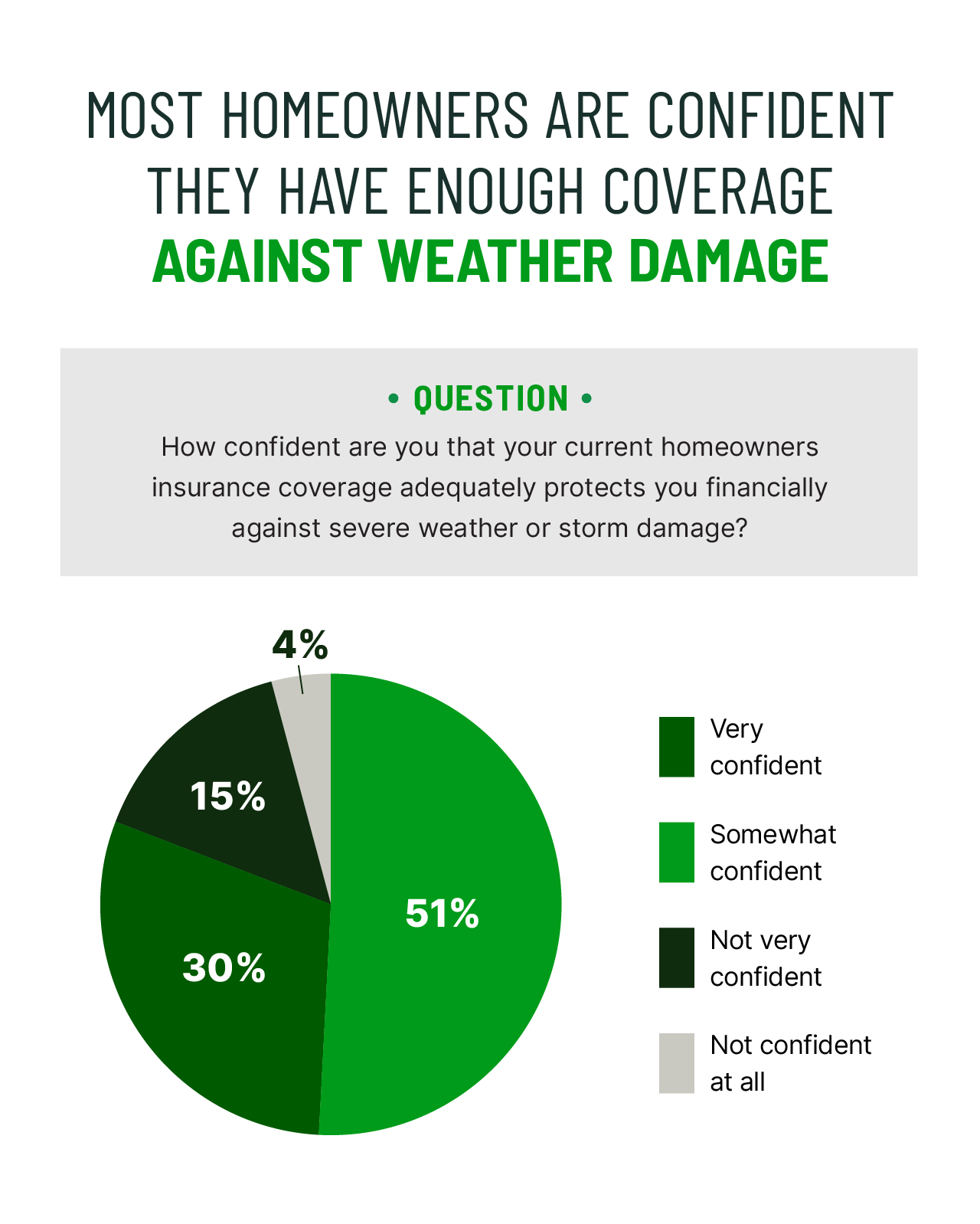

Homeowners may be overconfident about their homeowners insurance coverage when it comes to severe weather. Many homeowners (80%) are confident they have adequate coverage for severe weather or storm damage.

-

However, only 32% said they reviewed their homeowners insurance in the past year to understand their storm- and severe weather-related coverage.

-

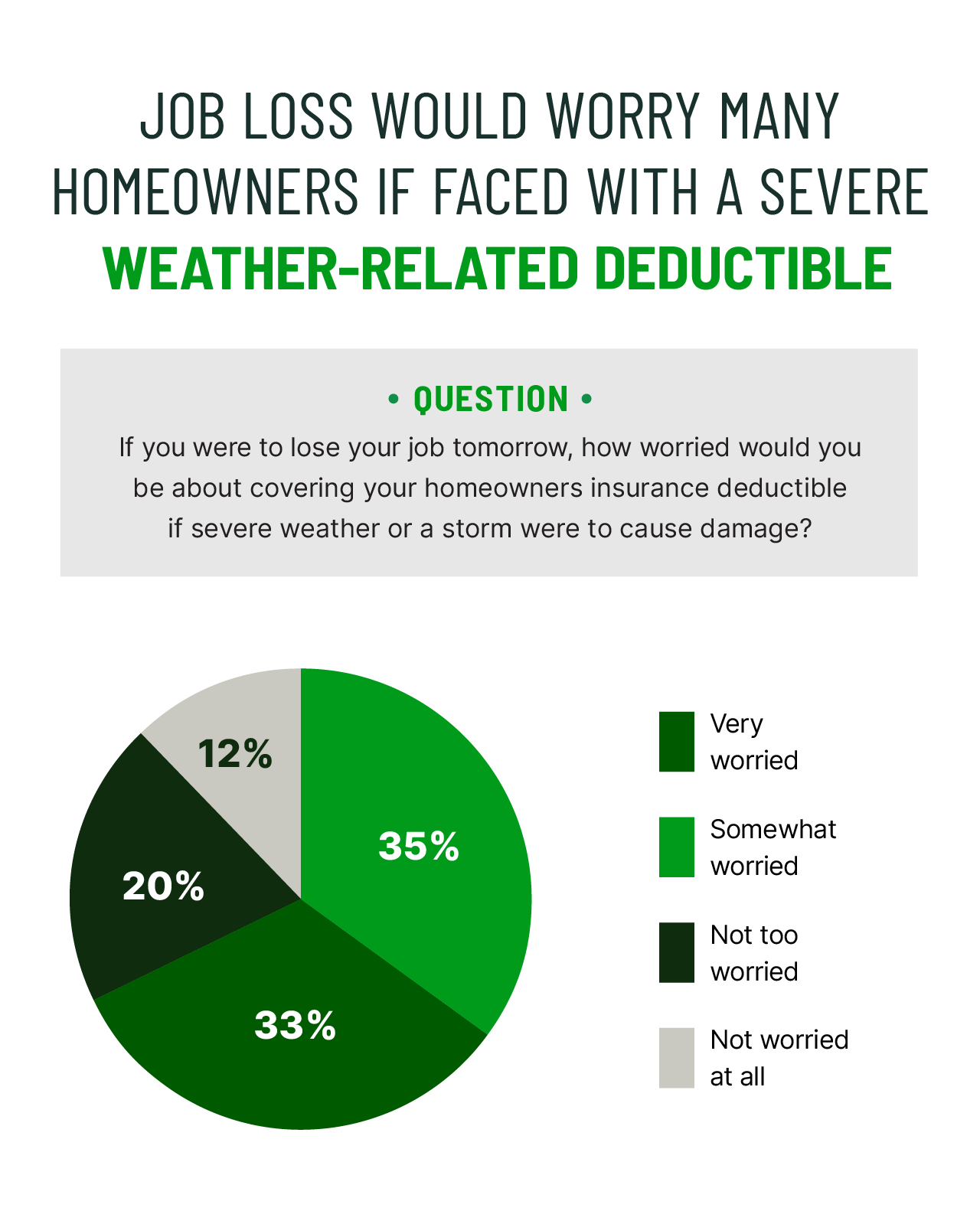

To make matters worse, job loss would make many homeowners (68%) worried about covering their homeowners insurance deductible if their home experienced severe weather or storm-related damage.

-

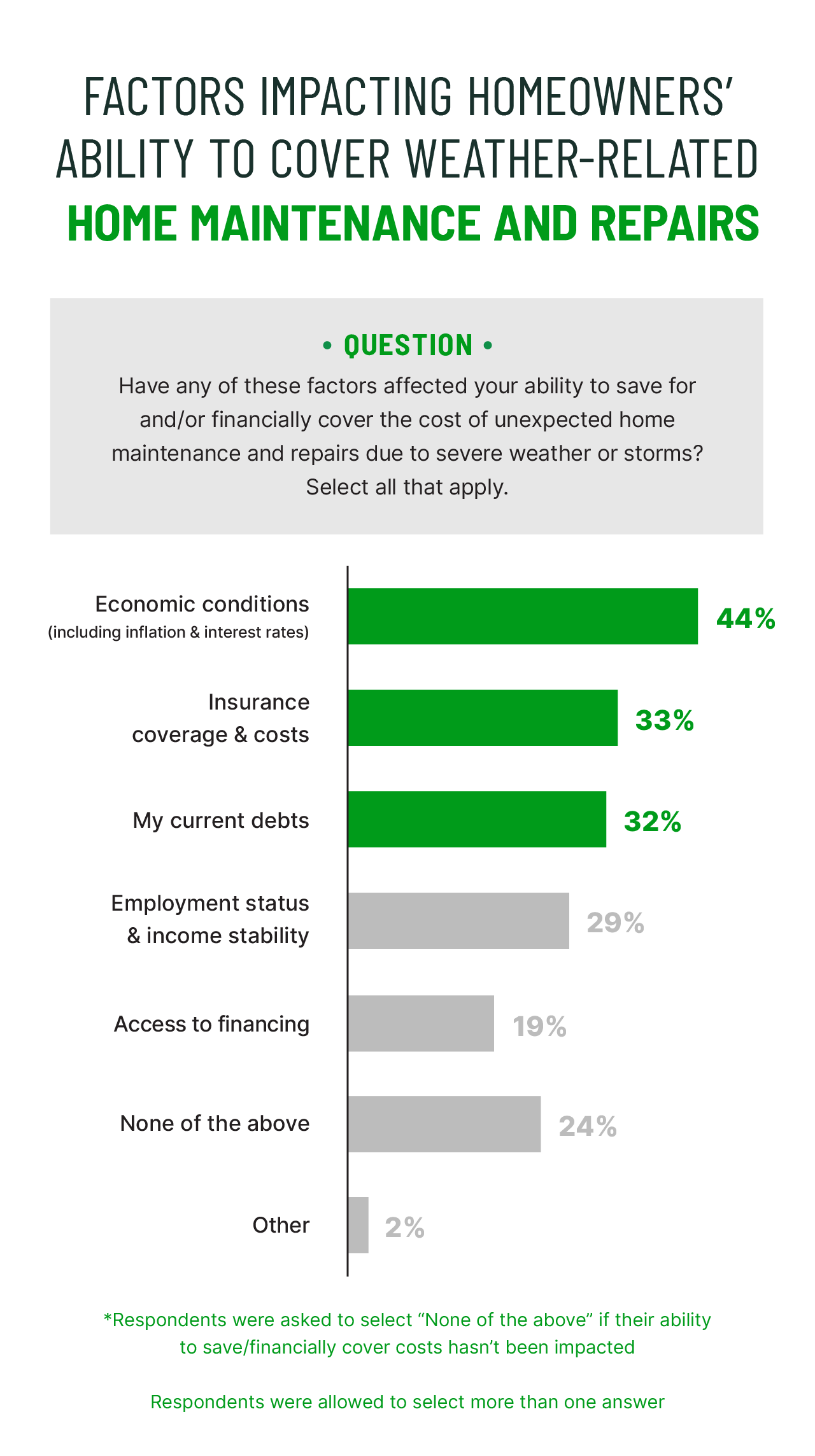

Homeowners are also struggling to cover unexpected severe weather costs because of economic conditions (44%), insurance costs (33%), and debt (32%).

-

Although some homeowners are taking steps to help protect their homes from severe weather and storms, strategies like taking a home inventory of their belongings (22%) and contributing to an emergency fund (30%) are low on the list of priorities for homeowners.

Most are confident in insurance coverage for storms, despite only 32% saying they’ve reviewed their coverage in the past year

More than 80% of responding homeowners said they were confident their current homeowners insurance policy could financially protect them against severe weather and storm damage.

However, only 32% of responding homeowners said they reviewed their homeowners insurance in the past year to understand what is and isn’t covered in case of severe weather or storms. Home insurance policies typically renew annually and your coverage can change between renewals.

Regularly reviewing your homeowners insurance can help you decide whether to adjust your coverage. This includes considering add-ons for certain types of damage from weather events you may not have anticipated when you first bought your home. If you didn’t initially consider the impact of these events, you’re not alone—52% of responding homeowners from our 2023 extreme weather survey also said they ignored severe weather risks when purchasing their homes.

Ignoring these threats may cost you if you experience a peril that your policy doesn’t cover. A peril is an event that can lead to loss of value or damage to your home. For example, flood damage isn’t typically covered by a traditional homeowners insurance policy, and you will need to purchase separate flood insurance.

Policy language can be complex, so it is recommended that you check with your insurance provider or agent about changes to your policy ahead of your home insurance renewal period. Below are a couple examples of coverage you may already have through your homeowners policy:

- Loss of use coverage provides financial assistance if your home becomes unlivable after a covered loss (like if a covered windstorm impacts your home)

-

Other structures coverage protects structures separated from your home (like sheds or fences)

However, homeowners policies have limitations. Below are additional types of severe weather-related coverage you can consider to help protect your home:

- Windstorm insurance provides coverage for high wind and hail damage

-

Extended replacement cost helps cover additional expenses associated with rebuilding your home above the coverage limit for your house

We recommend checking your homeowners insurance policy to learn about your current coverage. You can ask yourself the following questions below to help you consider factors that may have changed your coverage needs.

Adequate homeowners insurance is only one aspect for homeowners to consider when preparing their homes for severe weather. Everything from your income to economic conditions can make a difference in your financial preparations.

Job loss would cause more than 60% to worry about covering severe weather-related deductible costs

68% of responding homeowners said that job loss would make them feel worried about covering severe weather-related deductible costs.

Managing a home involves several ongoing expenses, ranging from your mortgage to ongoing maintenance and repairs.

Staying on top of those expenses may already feel like a challenge, but losing your main source of income can make it even more difficult to balance the financial demands of owning a home.

Today’s homeowners are already doing what they can to make their dollars count.

Our recent financial goals report found that 86% of responding homeowners say they’ve compromised on at least one area of their life to prioritize the costs of homeownership.

We also learned in that same survey that 44% of responding homeowners had $1,000 or less saved for home maintenance and upgrades. This may not cover major storm- or severe weather-related damage. For example, one inch of flood water can cause close to $25,000 of damage to your home, according to the Federal Emergency Management Agency (FEMA).

Job loss can exacerbate an already pricey scenario if your home experiences severe weather damage.

Economic conditions, insurance, and debts are the top financial barriers for homeowners

Responding owners ranked economic conditions (44%), insurance coverage and costs (33%), and debts (32%) as the top factors that impacted their ability to save and/or financially cover the cost of unexpected home maintenance and repairs due to severe weather or storms.

January 2024 saw a .3% increase in the consumer price index (CPI). Motor vehicle insurance, tenants’ and household insurance, and health insurance are among the costs that rose (U.S. Bureau of Labor Statistics).

Rising costs can happen for many reasons that are out of our control. Even if you don’t file a claim, your homeowners insurance costs can increase if your natural disaster risk increases or if the cost of materials or labor increases.

The Congressional Budget Office recently projected that economic growth will slow in 2024 as unemployment increases (influenced partially by tight monetary policy). They also reported that total consumer debt reached the highest level ever recorded—116% of the GDP (Congressional Budget Office, February 2024).

The average homeowner could feel the impact of these factors when making everyday decisions with their budget. Increased insurance costs could mean they’ll have less money available to tackle a minor repair. Sudden severe weather events can also complicate a homeowner’s tight budget.

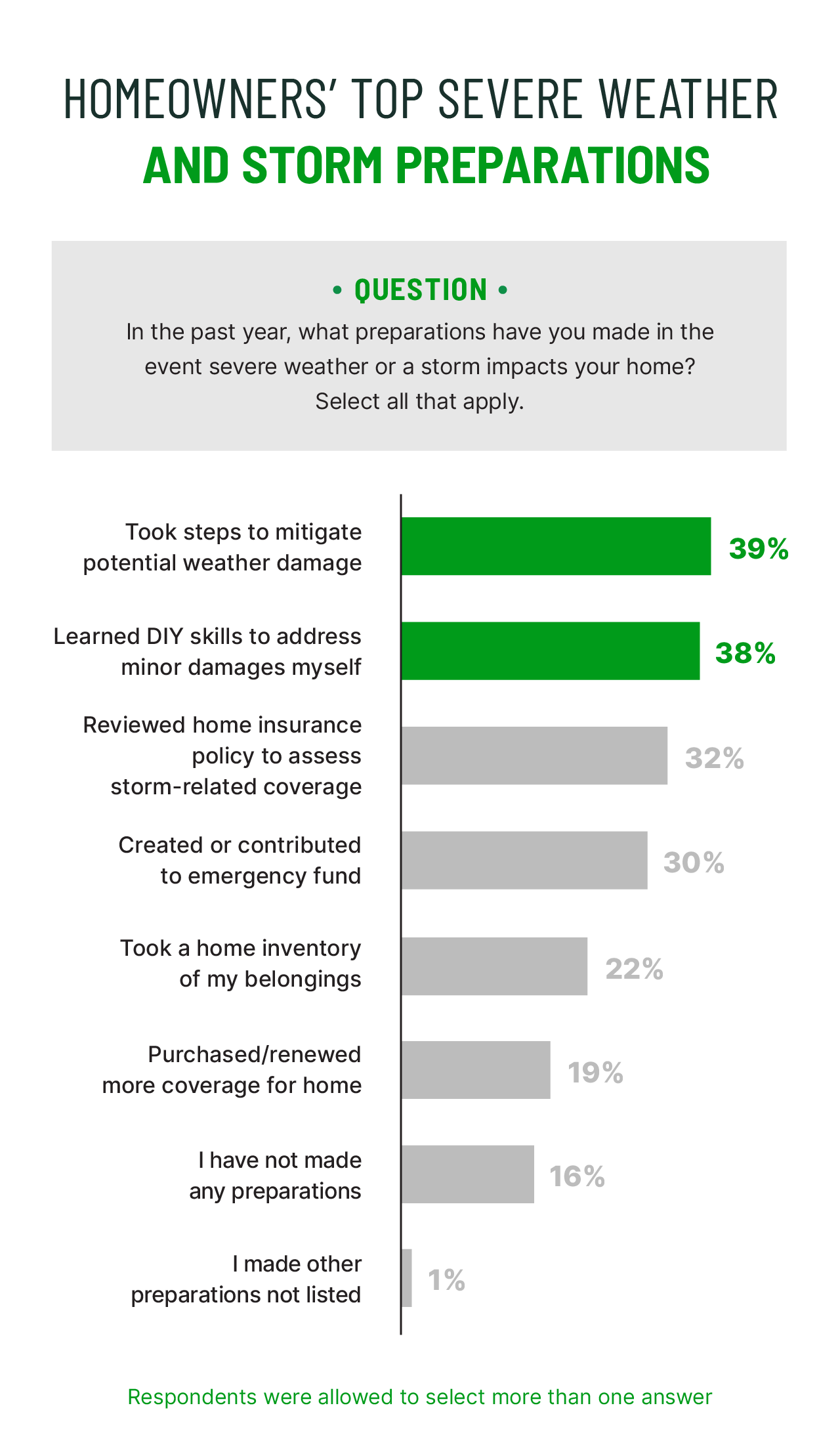

Homeowners are taking some steps to protect against severe weather—but could be doing more

We asked homeowners what preparations they made in the past year in the event severe weather or a storm impacted their homes.

Less than half (39%) of responding homeowners took steps to mitigate potential weather damage, like trimming trees and checking for drainage around the home. Addressing risks before a severe weather event can help prevent future issues. For example, removing overhanging tree limbs near your roof can help prevent roof damage.

Less than half (38%) of responding homeowners also said they learned basic DIY maintenance and repair skills to address minor damage themselves. Although it’s better to leave complex tasks, like extensive roof repairs, to the pros, you can make some minor preparations by yourself. This can include visually inspecting your roof for damage and cleaning your gutters before a storm.

Other tasks, like contributing to an emergency fund (30%) or taking a home inventory (22%), can help you financially prepare for potential damage.

While sufficient insurance coverage can help you financially recover from severe weather events, preventative maintenance can help minimize the potential damage in the first place.

For example, if your roof is missing some shingles, it may be more susceptible to water penetration during heavy rain. Replacing a few shingles can be a relatively small job compared to a roof replacement, depending on the extent of the damage.

The free Hippo Home app can help you keep track of preventative tasks like these by providing a personalized checklist for your home and built-in reminders to get them done. You can also access DIY guides for help addressing tasks on your own.

Learn more about Hippo Home today to learn how you can help proactively protect your home.

Methodology

The survey was conducted by SurveyMonkey Audience for Hippo Insurance Services. The survey was fielded between February 8, 2024, and February 9, 2024. The results are based on 1,120 completed surveys. In order to qualify, respondents were screened to be residents of the United States, over 18 years of age, and own a home. Data is unweighted, and the margin of error is approximately +/-3% for the overall sample with a 95% confidence level.

Disclaimers

YourHaus, Inc. ("Hippo Home") is an affiliate of Hippo Insurance Services. Services (including all repair or maintenance services) provided to customers through affiliated and unaffiliated third-party contractors. Your use of Hippo Home is subject to Hippo Home's terms and conditions and privacy policies. Use of unaffiliated third-party vendors is subject to the terms of service provided by such third party. Hippo Insurance Services is not responsible for your use/non-use of Hippo Home or any service vendor. @ YourHaus, Inc. 2023

Hippo Insurance Services ("Hippo") is a general agent for affiliated and non-affiliated insurance companies. Hippo is licensed as a property casualty insurance agency in all states in which products are offered. Availability and qualification for coverage, terms, rates, and discounts may vary by jurisdiction. We do not in any way imply that the materials on the site or products are available in jurisdictions in which we are not licensed to do business or that we are soliciting business in any such jurisdiction. Coverage under your insurance policy is subject to the terms and conditions of that policy. Coverage and coverage amounts selected are the decision of the buyer.

This guidance and advice is not error-proof and not applicable to every home. You are responsible for determining the proper course of action for your property and neither Hippo nor Hippo Home is responsible for any damages that occur as a result of any advice or guidance.