Why Did My Homeowners Insurance Go Up?

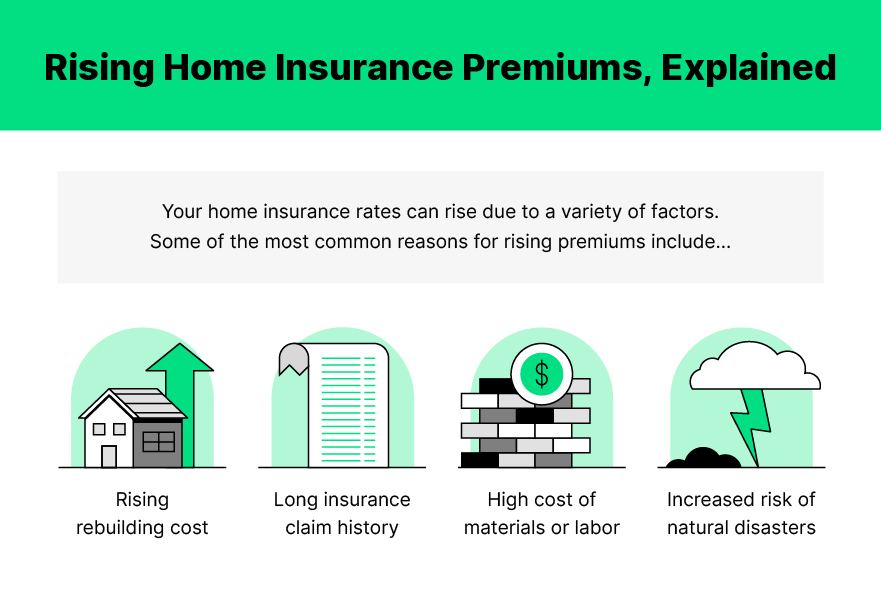

Homeowners insurance rates can go up for a variety of reasons, including rising rebuilding costs, a higher price tag on materials or labor, your home has reached a certain age, you’ve submitted several claims in the last year or your natural disaster risk has increased. But if your premiums rise, don’t fret just yet.

Not all the reasons behind a spike in premiums are negative; for example, you can also expect to see a slight increase in your rate if your property value has increased significantly over the past year. If this is the case, your premium only rises to make sure you have the full protection you need.

Your home insurance can go up due to a variety of factors, including:

- A rise in rebuilding costs, such as materials or labor

- The age of your home

- Your claim history

- Natural disaster risk

- A rise in property value

- Addition of high-risk items, like a pool or trampoline

First things first: If you get your new insurance bill and it's higher than what you're used to, don’t panic. Your insurance provider has got your back, meaning the likely reason your rate rose in the first place is to ensure you are completely covered. After all, that’s why you bought a policy, right?

Below, you can learn more about rising premiums, how to talk to your insurance provider about them and what you can do to get that cost down without becoming underinsured.

Is homeowners insurance going up in 2022?

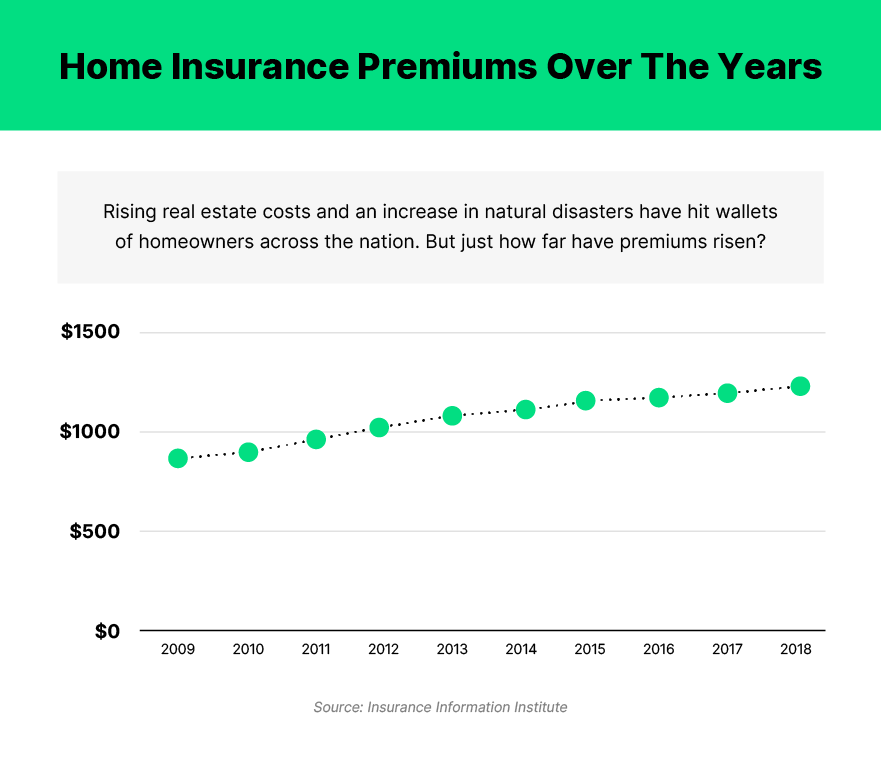

On average, homeowners insurance costs have gone up 4% each year since 2009, an increase you can expect to continue from 2021 to 2022. This steady increase is due to several factors, including an increase in natural disasters across the board, rising property values in popular cities like Austin (or the many others that fall into this category) and older homes experiencing age-related issues.

How to talk with your insurance provider about rising premiums

It can be tempting to lower your coverage levels to save yourself some cash when you get that home insurance bill with elevated premiums. But don’t slash and burn just yet, as you might accidentally render your coverage pointless if you make too many cuts. Instead, work with your insurance provider to learn exactly why your premium increased and what you can do to change it, so you can still save money without risking your home’s protection.

Questions to ask

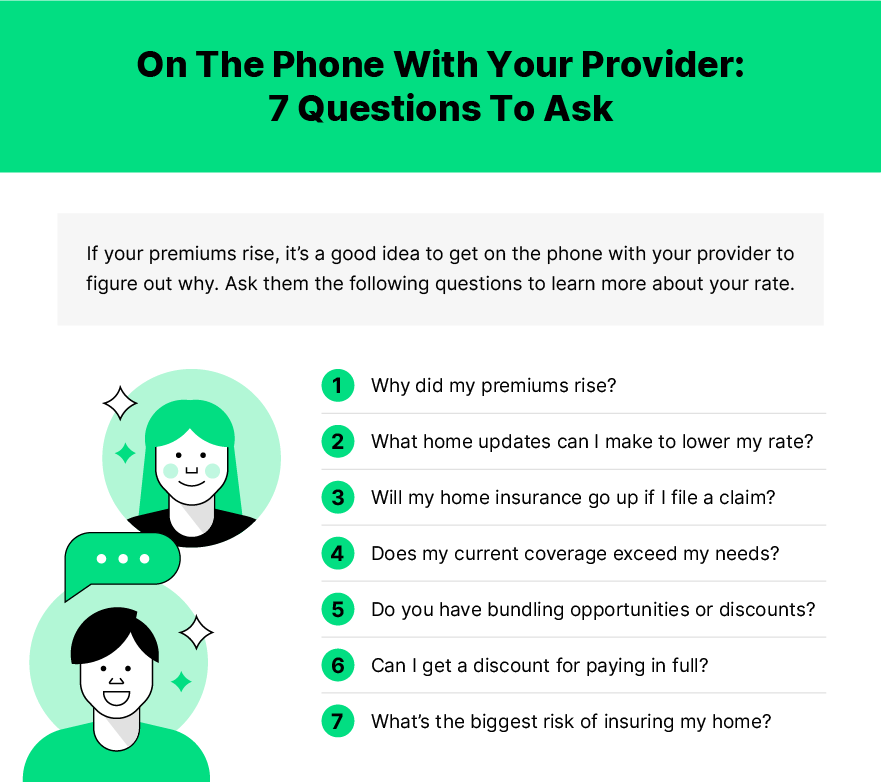

Talking to your provider may seem fruitless, but depending on who you signed a policy with, you may find them more helpful than you think. Ask your insurance agent the following questions when trying to determine why your premiums rose — and what you can do to lower that cost. They’ll likely help you get to the root of the problem and figure out a plan forward.

- Why did my premiums rise?

- What updates can I make to my home to lower my premium?

- Will my homeowners insurance go up if I file a claim?

- Does my current coverage exceed my home’s needs?

- Do you have bundling opportunities or offer any discounts?

- Can I get a discount for paying my premium in full?

- What do you see as the most significant risk of insuring my home, and what can I do to lower that risk?

Your coverage options

If your insurance premium rose this year, should you really consider adding on more coverage? The answer is: It depends. While adding on more coverage when trying to get your premium down may seem counterintuitive, if your rates rose due to rising material or labor costs, adding more coverage now will save you a lot of money down the line. This is especially true if you have to repair or rebuild a large portion of your home, or you have an older home that needs to be brought up to code.

Adding on various insurance riders like extended replacement cost and building ordinance or law coverage can be an excellent way to save yourself a lot of money in the long run, even if it means spending a little more upfront. To determine the best insurance riders for your home’s unique needs, make sure to talk with your insurance agent about your options.

Another factor worth considering is the natural disaster risk in your area. If you haven’t lived in your city for long, research what disasters are common in your climate and how often they occur. Then, you can add on the proper insurance riders (think: hurricane insurance on the coast or wind insurance if you live in tornado alley) to stay protected no matter what storm comes your way.

Insider tips for lowering your homeowners insurance

No matter what type of home you own — or how old it is — there are things you can do to get your insurance premiums down. While discounts and bundling opportunities will vary by provider, try out the following tips to save a little extra on your next home insurance premium.

- Take steps to improve your insurance score.

- Build a good credit history.

- Pay your bills on time.

- Upgrade your home to make it safer, smarter and more streamlined.

- Install smart home monitoring devices.

- Add a security system.

- Upgrade outdated portions of your home, such as the HVAC system or the roof.

The age-old saying “You get what you pay for” is popular for a reason — it’s often true. By working with a modern provider and adding some smart upgrades to your home, you just might be able to get your premium down without sacrificing coverage. Give us a call to chat through your home’s unique needs and learn about our free smart home kits. They’re just one of the many ways we’re dedicated to helping you save.