The best way to evaluate your next home insurance policy

Most homeowners can agree that insurance is a necessity, whether it’s for offering protection, providing peace of mind or simply because mortgage lenders require it. Having coverage isn’t nearly enough, though. You want to make sure you have the right coverage at the right cost, which is why it’s important to check your policy at least annually. Luckily, most providers send a renewal statement once a year before your policy is scheduled to expire.

Some people just confirm the address, sign on the dotted line and send the renewal statement back, but you shouldn’t just assume your existing policy is your best option. Renewals provide the perfect opportunity to evaluate how your insurance needs may have changed, whether your coverage is adequate, if you’re satisfied with your current provider and how you may be able to save more on your premiums. After all, it’s unlikely that you’re in the same position now as when you first bought your home or last checked your policy. The following are factors that should be considered when you review your policy.

Coverage

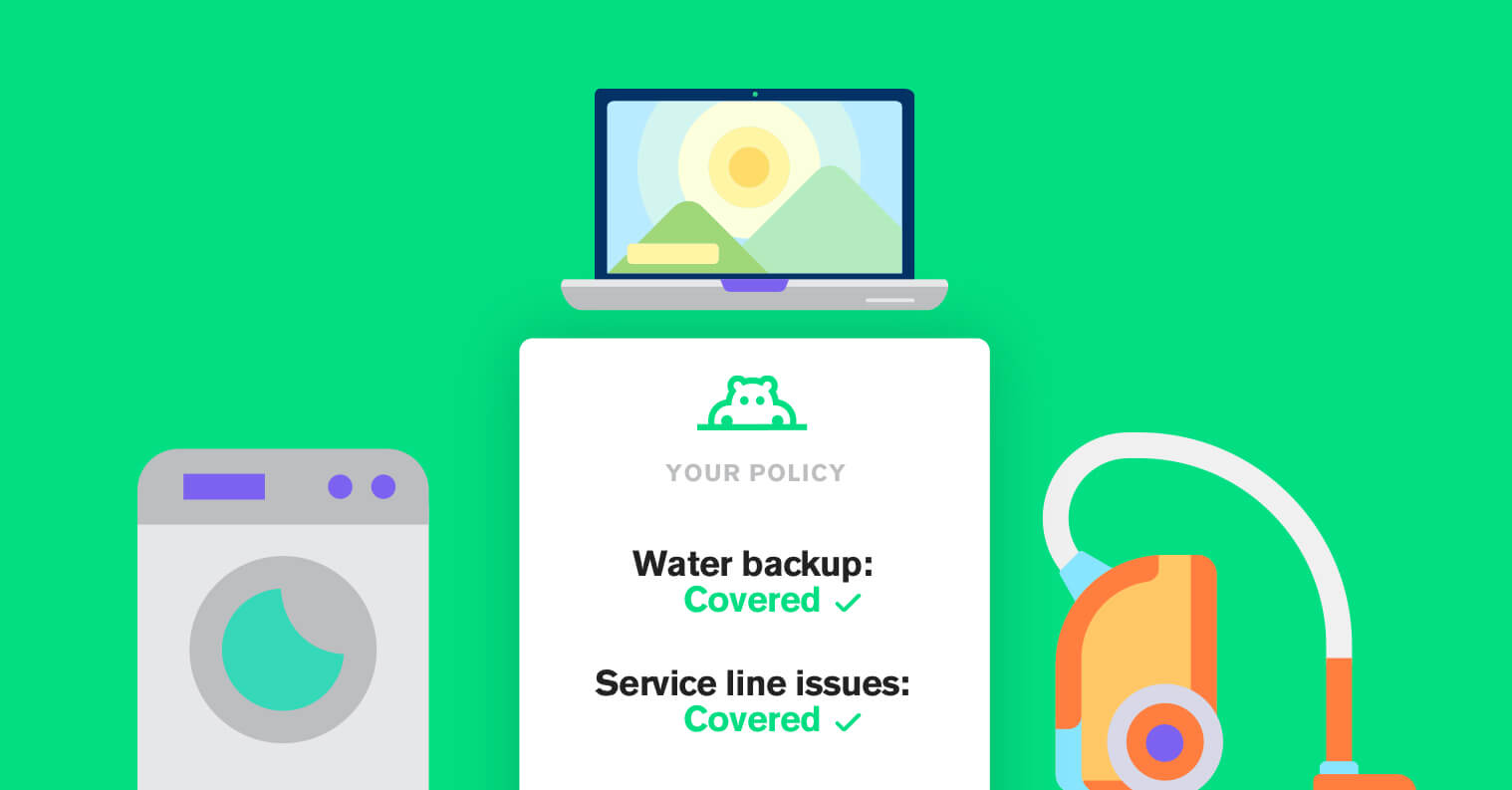

Truly, the most important thing is being adequately covered. About two-thirds of U.S. homes are underinsured, meaning homeowners could incur financial hardship despite feeling protected by their insurance policy. There are four main coverages that policies tend to include: dwellings, personal property, additional living expenses and liability. Consider what events you’re currently covered for and what other disasters you may be susceptible to. It’s also a good idea to look at insurers that provide for loss and damage that other providers don’t. For instance, Hippo covers water backup and service line issues.

Renewal statements also provide the chance to take stock of what you own. A video inventory is the best way to record your assets. You may be surprised what’s left out of standard policies and requires scheduling and additional coverage

Costs

Premiums are rising nationwide as a result of an increase in natural disasters, claim severity and construction costs. Some homeowners are experiencing rate jumps despite never filing a claim or missing a payment. While there’s no rule of thumb for how much you should pay in homeowners insurance premiums, home age, home size, home location and your creditworthiness are all part of the calculation. Every state is different and it’s best to compare locally but the Insurance Information Institute has found that the average annual premium in the U.S. was $1,173 in 2015, the most recent year for available data.

When comparing your options, it’s also important to be sure you’re getting homeowner insurance quotes for the same (or better) coverage than you currently possess. You can also consider whether your deductibles are actually sustainable. Raising it could lower your monthly or annual premium, but that means you’ll have to pay more out-of-pocket when disaster strikes.

Discounts

Luckily for most homeowners, there’s more to the cost of your premium than your quote. Many organizations and actions can help you score a significant discount. Think bundling policies, paying off your mortgage or belonging to an affinity group discount (employer, university, homeowners association, etc.). Sometimes, even just staying with the same insurance company for several years can lead to savings of up to 10%.

When you find out the cost of your renewed policy, it’s wise to check whether you could qualify for any additional reductions. Not all providers will tell you about these options upfront so you may have to inquire about availability or qualification requirements.

Service

If you have filed a claim since you last reviewed your policy, consider that experience. A lower price and adequate coverage are certainly important but you also want to be satisfied with customer service when you need to make use of your insurer (which hopefully isn’t too often). Think about how efficiently and appropriately the claim was handled, whether you were contacted in a timely fashion and if you got the empathy and support you needed.

If you haven’t had any events during the policy life, it can be more difficult to gauge the quality of your insurer’s service. Check online resources and ask your friends or family about their insurers to determine who has a good reputation among policyholders.

Relationship

Even if you haven’t had to file any claims recently (or ever), a renewal offers the chance to think about what your insurance provider really does for you. Do you know and feel comfortable with your agent? Do they provide helpful resources or can you reach out and easily get in touch with someone? Many newer insurance companies have changed the business model to operate with bots, which works for some people but doesn’t for others.

On the other end of the spectrum, providers like Hippo are working to become a proactive partner in the safety of your home and family. They provide an open line of communication and offer perks like IoT devices that detect danger and minimize your home’s risks. Some even use real-time intelligence to ensure policyholders know about impending danger and have the support they need in the wake of a crisis.

Timing is everything

Annual renewal is definitely a crucial time to review your insurance policy, but you should also look it over whenever you experience a major life change. Whether you welcome a new family member or start a new job, your insurance needs or budget might change. Just make sure you think holistically and consider all five of the above factors when you evaluate.

If you do decide to switch policies or insurance companies, make sure you act quickly. You want to solicit premium quotes at least one month before your current policy expires so you can secure a new policy without experiencing a gap in coverage and possible out-of-pocket damage or loss expenses.