AI adoption study: The growing generational divide in home insurance

As AI becomes a part of everyday tasks and routines, home insurance is no exception. AI is streamlining claims processing, helping carriers assess risk more accurately, and giving homeowners new tools to research coverage options and understand what’s available to them before making a policy decision.

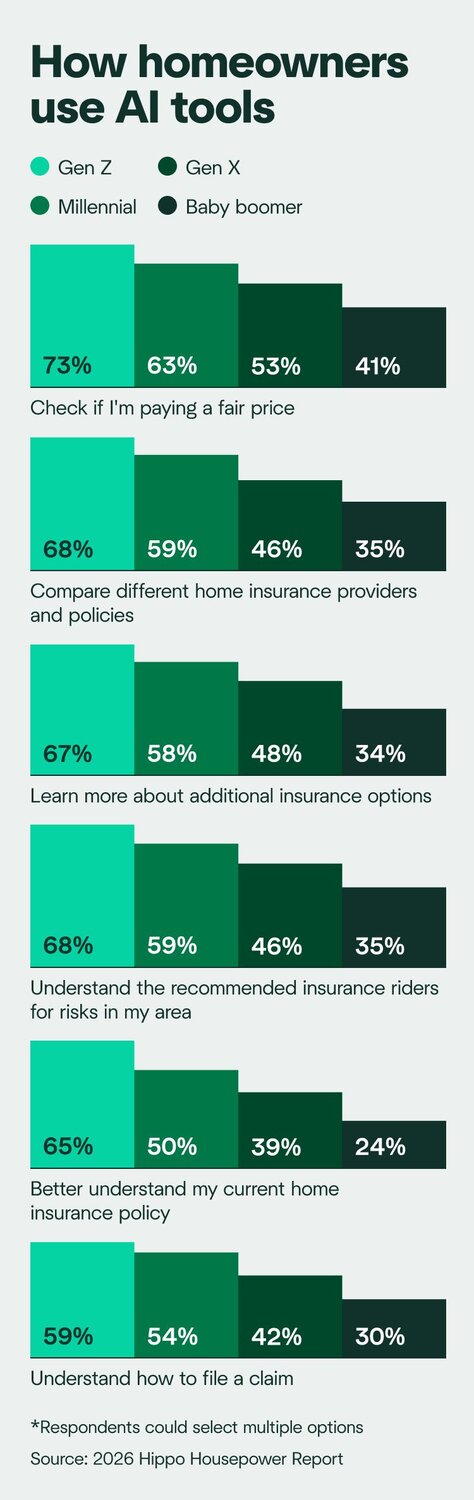

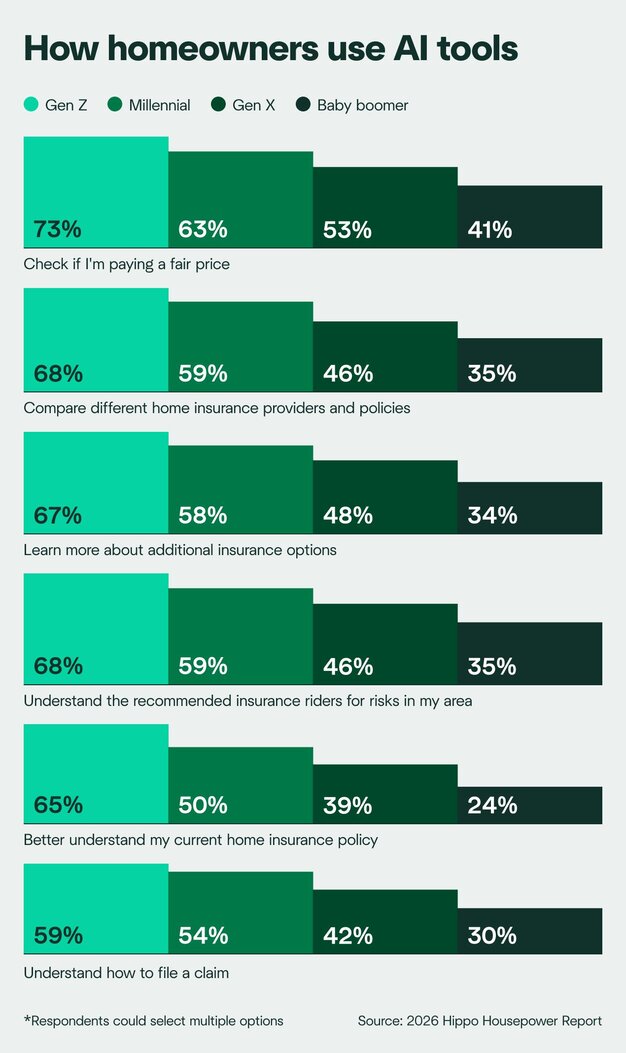

Still, not all homeowners are adopting AI at the same pace. According to the 2026 Hippo Housepower Report, 65% of Gen Z homeowners expect to use AI in 2026 to better understand their current home insurance policy, compared to 24% of baby boomers.

As more homeowners turn to AI for insurance research, it’s worth knowing how to use it safely and effectively. Below, we explore how homeowners are putting AI to work, and what to keep in mind along the way.

Key takeaways

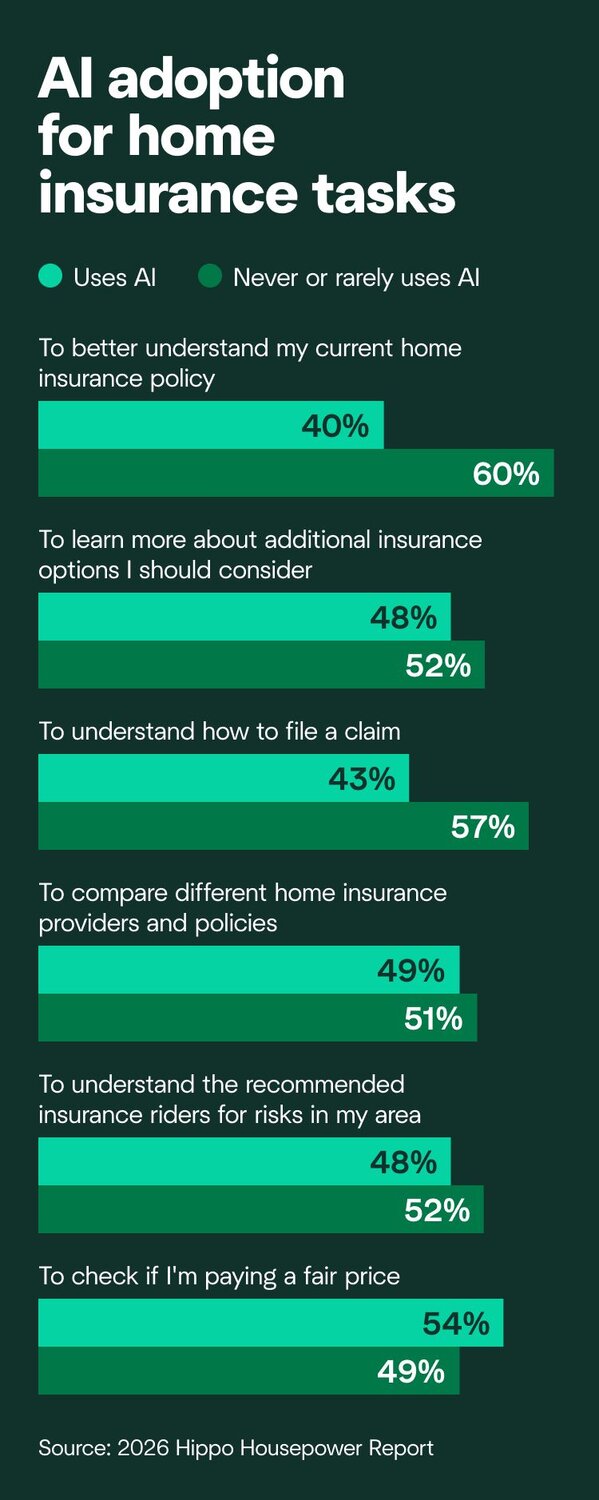

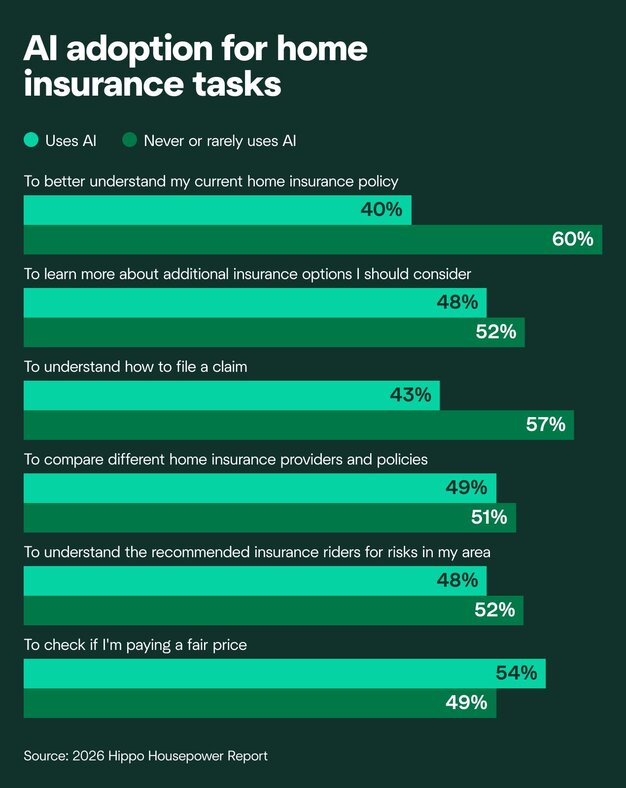

- Insurance decisions can be complex. To make them easier, homeowners are turning to AI tools for tasks like researching if they’re paying a fair price (54%), comparing insurance providers and policies (49%), exploring additional coverage options (48%), and understanding their current policy (40%).

- Gen Z and Millennials increasingly turn to AI for policy research, claims guidance, and cost comparisons. Boomers and Gen X are more likely to stick with traditional research channels.

- When baby boomers use AI for home insurance research, their most common reason is to check if they're paying a fair price—less than half (41%) plan to do this in 2026, compared to 73% of Gen Z homeowners.

More than 1 in 2 homeowners use AI to see if they're paying a fair price for home insurance

U.S. homeowners overwhelmingly plan to use an AI tool (like ChatGPT or Google Gemini) in 2026 for home insurance-related research.

Specifically, homeowners say they will use AI at least sometimes to:

- Check if they're paying a fair price (54%)

- Compare insurance providers and policies (49%)

- Explore additional coverage options (48%)

- Better understand their current policy (40%)

- Understand how to file a claim (43%)

- Learn more about insurance riders for risks in their area (48%)

This high percentage of homeowners focused on price suggests that many homeowners are concerned about insurance costs. Climate change, higher home values, and the rising cost of building materials have contributed to homeowners' insurance rates rising nearly 70% on average since 2020.1 And with 42% of younger working Americans living paycheck to paycheck,2 it makes sense that younger homeowners are looking for every tool available to help them find insurance discounts and affordable coverage.

That said, while AI can make research quicker and easier, it works best as a starting point and not the only source of information for insurance decisions. For coverage decisions, it's best to consult a licensed insurance producer.

Gen Z is quick to use AI to find the right insurance

Nearly half (47%) of Gen Z homeowners already use AI weekly for everyday tasks—and they're bringing that habit to homeowners insurance.3 According to the 2026 Hippo Housepower Report, Gen Z homeowners are quite comfortable using AI for insurance questions in 2026:

- Price checking tops the list: 73% expect to use AI to see if they're paying a fair price–the most common use case across all generations.

- Coverage research also ranks highly: 67% plan to learn more about additional coverage options, 65% want to better understand their current policy, 66% are researching recommended insurance riders for regional risks, and 68% plan to compare providers and policies.

- Claims questions appear slightly less urgent: 59% of Gen Z homeowners plan to use AI to understand how to file a claim, suggesting this generation is more focused on affordability than proactively addressing the claims processes until they need it.

Unlike Gen Z, baby boomers are much less likely to use AI for basic home insurance questions. Only 24% plan to use AI to better understand their current home insurance policy, and only 30% plan to use it to understand how to file a claim. Having owned homes and carried insurance for longer, older generations may simply feel more confident navigating these questions on their own.

Majority of Gen Z will use AI to prepare for local risks

Choosing the right policy and riders (add-on policies) means weighing different variables. AI can help homeowners start to narrow choices based on local climate risks. In fact, 66% of Gen Z homeowners plan to use it to understand recommended riders for their area.

That focus on climate risk aligns with broader preparedness trends. Gen Z homeowners are more likely than baby boomers to proactively prepare for home emergencies or extreme weather. The 2026 Hippo Housepower Report found 86% of Gen Z plans to prepare for extreme weather in 2026, compared to only 68% of baby boomers. The difference shows up clearly in the specific actions each generation plans to take:

Action | Gen Z homeowners | Baby boomer homeowners |

|---|---|---|

Create an emergency plan (e.g., evacuation route, supplies) | 36% | 28% |

33% | 8% | |

Review home insurance coverage | 39% | 28% |

Install more home protection equipment (e.g., sump pump, smoke alarms) | 34% | 13% |

Set aside an emergency fund specifically for home repairs | 38% | 26% |

Gen Z tends to be more climate-conscious than older generations.4 High-profile events like the 2025 Los Angeles wildfires and winter storm Fern might be top of mind as many in this generation face extreme weather for the first time as homeowners.5,6

AI prompts for home insurance research

AI can be useful early in the home insurance process, especially when you’re not sure where to start or what questions to ask a licensed home insurance producer.

If you already have a policy, you can upload basic information like your coverage type, limits, deductibles, and exclusions to a free tool like Gemini or ChatGPT and ask it to summarize key coverage details.

Never share personal details like your full name, contact information (like email or phone number), home address, bank account information, or credit card numbers.

If you're starting without a policy, AI can help define insurance terms, explain coverage basics, or help you think through how much coverage you might need. The prompts below can help you begin your research. Just make sure to double-check your questions and answers. AI might not always catch typos and it may make mistakes itself.

Understanding an existing policy or how to file a claim

If you already have a policy, AI can help act as a translator for the dense legal language. While it’s still important to get clarity from a licensed insurance producer before making coverage decisions, these prompts can help provide information about the core protections of a policy and the logistical steps of a claim.

Prompt for identifying core coverage areas:

I am buying my first home. In simple terms, what are the five main things a standard home insurance policy protects? Does it cover the house itself, my stuff inside, and what happens if someone gets hurt on my property? Please cite your sources.

Prompt for comparing deductible options:

Explain how home insurance deductibles work. If I choose a [amount] deductible versus a [amount] deductible, how can that change my monthly premium? What are the pros and cons of having a high deductible as a new homeowner with limited savings? Please cite your sources.

Prompt for creating a claims checklist:

I recently experienced [type of home damage]. I need to file a claim with my insurance company, [name of insurance company]. Create a step-by-step checklist of what I should do before, during, and after calling [name of insurance company]. Include advice on how to document the damage and what questions I should ask the adjuster when they arrive. Please cite your sources.

Researching risks that could require additional coverage

These prompts can help you identify which coverage options may apply to your situation, so you can have a more informed conversation with a licensed insurance producer.

Prompt for choosing common insurance riders:

I am a homeowner in [city/state]. My home was built in [year]. Based on my location and home age, what are the most common insurance riders I should consider to cover gaps that a standard policy may exclude? Please cite your sources.

Prompt for comparing endorsements to a standard policy:

I have my insurance declarations page. I am going to paste the “Endorsements” section here. Please compare this to a typical comprehensive homeowners policy in my area. Please cite your sources. [your policy’s endorsements details]

Prompt for reviewing local environmental risks:

Act as a local risk assessment expert for [your zip code]. What are the most common causes of property insurance claims in this specific area? Based on these risks, what specific insurance riders (like flood, earthquake, or windstorm) would you recommend I ask my agent about? Please cite your sources.

Finding the best price or home insurance discounts

These prompts can share useful information about pricing factors, discounts, and optional coverage to help you go into conversations with producers better prepared.

Prompt for evaluating premium costs:

I live in [your zip code], and my annual home insurance premium is [amount]. My home is worth approximately [estimated value] and was built in [year]. What affects the cost of my home insurance premium? Please cite your sources.

Prompt for evaluating insurance bundling:

I currently have car insurance with [company]. What are the typical benefits of 'bundling' my new home insurance with my existing auto policy? Are there any situations where it might actually be cheaper to keep them separate? Please cite your sources.

Prompt for comparing insurance quotes:

I have two home insurance quotes. Quote A is from [company] and Quote B is from [company]. Quote A is more expensive than Quote B. I am going to paste the 'Coverage Summary' for both below. Please create a table comparing the Dwelling Coverage, Personal Property, Liability, and Deductibles. Highlight any differences in what is not covered (exclusions) between the two. Please cite your sources.

Remember: AI tools can provide helpful guidance, but may occasionally be inaccurate or biased. AI is not a replacement for making decisions yourself, it supports making sounder decisions. For insurance choices, it’s best to seek advice from a licensed insurance producer.

Ready to learn more about home insurance? Start with Hippo Insurance Services

AI is already reshaping how homeowners think about and research insurance–and it will keep evolving the way we protect our homes and families. The more you understand your home’s needs, the better positioned you’ll be to make confident decisions about protecting what matters most. When understanding your home insurance options feels overwhelming, Hippo can help. Check out your home insurance options today.

Methodology

Any data referencing the 2026 Housepower Survey was collected on September 22, 2025, and conducted by Centiment on behalf of Hippo Insurance Services. The results are based on 1,619 completed surveys. In order to qualify, respondents were screened to be residents of the United States, over 18 years of age, and homeowners. Data is census-balanced, and the margin of error is approximately ±2% for the overall sample with a 95% confidence level.

The MOE and confidence level for data filtered by specific demographics (subgroups) may differ from the overall result. Because these subgroups are naturally smaller than the total sample, they may have a larger margin of error than the ±2% for the full data set.

External sources

- CBS News. (2025) Homeowners insurance costs have shot up 70% since 2021. Here's why.

- CBS News. (2025) More Americans are living paycheck to paycheck, putting retirement out of reach, report finds

- Walton Family Foundation-Gallup (2025) Gen Z Is Using AI — But Reports Gaps in School and Workplace Support

- Pew Research Center. (2021) Gen Z, Millennials Stand Out for Climate Change Activism, Social Media Engagement With Issue

- UN Office for Disaster Risk Reduction. (2026) The invisible costs of wildfire disasters in 2025

- Barron’s. (2026) Winter Storm Fern Packed a Wallop. Now the Cost Estimates Are Rolling In

This article is for informational purposes only. The content reflects general homeowner considerations and is not professional advice. It also includes observed trends within the surveyed population and certain additional information compiled from sources not affiliated with Hippo. While we believe this information to be reliable, we do not guarantee its accuracy or completeness. For any insurance-related decision, please consult your licensed insurance producer.

Sources cited are publicly available and referenced in February 2026.

Related articles

Hippo Housepower Report: Homeowners Gain Ground, Face New Challenges in 2026

Personalization in Homebuilding: Leveraging AI to Sell More Homes

Young Homeowners Fear Natural Disasters Most, Despite Preparation

Homeowner's Guide to Extreme Weather in 2026: What's Next and How To Prepare

52% of Homeowners Ignored Extreme Weather Risks Before Buying—Now Emergency Funds Are at the Forefront