Homeowner's Guide to Extreme Weather in 2026: What's Next and How To Prepare

As 2025 wraps up, you're probably thinking about next year’s routine home tasks—cleaning gutters, changing filters, and maybe finally fixing that leaky faucet. But one task deserves a higher spot on your list: preparing for severe weather.

Wildfires, hurricanes, and other dangerous weather events are becoming more common.1 In fact, 84% of homeowners experienced more weather-related challenges in 2024, including flood or wildfire risks, hail storms, or hurricanes, according to our 2024 Housepower Report.

Yet, at the same time, only 33% of homeowners made home improvements to reduce severe weather risks in the last year, down from 39% in 2024, according to our 2025 Extreme Weather Survey.

This guide explains how extreme weather affects homes in different U.S. regions, how homeowners can prepare, and the steps to take after a storm.

Key takeaways

- In 2025, 33% of homeowners said they made home improvements in the last year to reduce severe weather risks, down from 39% in 2024.

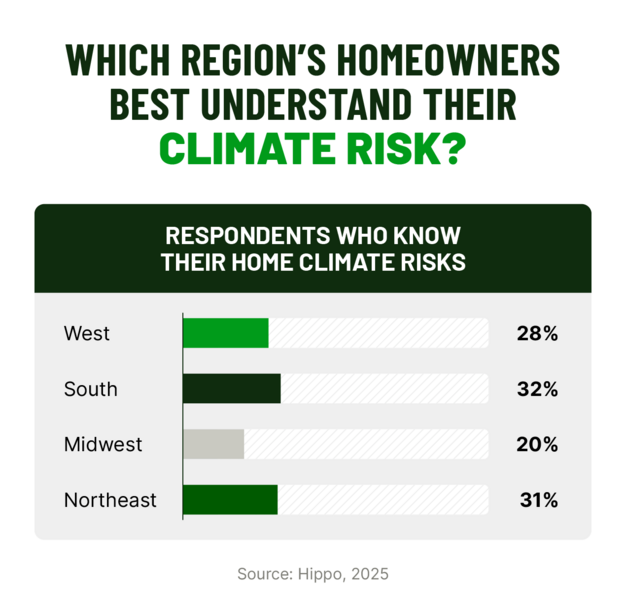

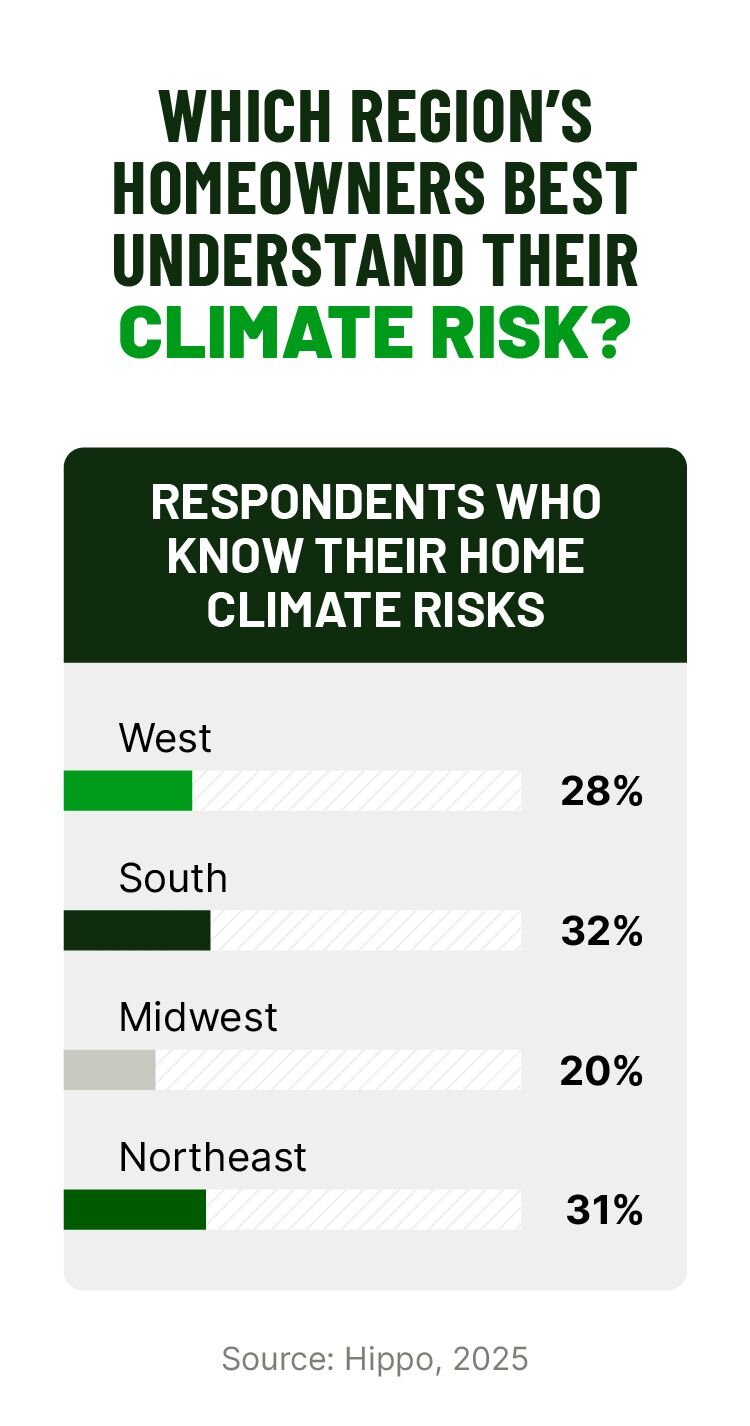

- Western homeowners were the most likely to prepare for severe weather. 37% took steps to mitigate potential weather damage in the last year.

- 46% of homeowners spent more than $5,000 out of pocket on unexpected home repairs in 2024, up from 36% in 2023.

- More than 1 in 5 homeowners say cost is the main barrier to weather-proofing their home.

Western homeowners lead in extreme weather protection

While outliers exist, extreme weather events affect some areas of the U.S. more than others. And according to our Extreme Weather Survey, most U.S. homeowners say they have taken at least one action to prepare, like contributing to an emergency fund.

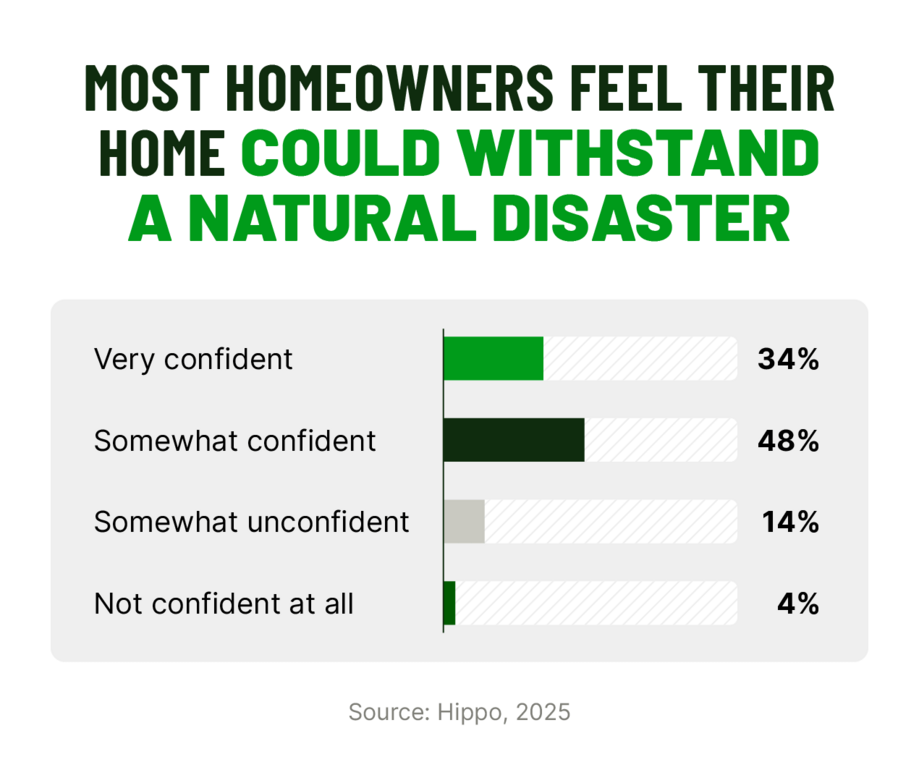

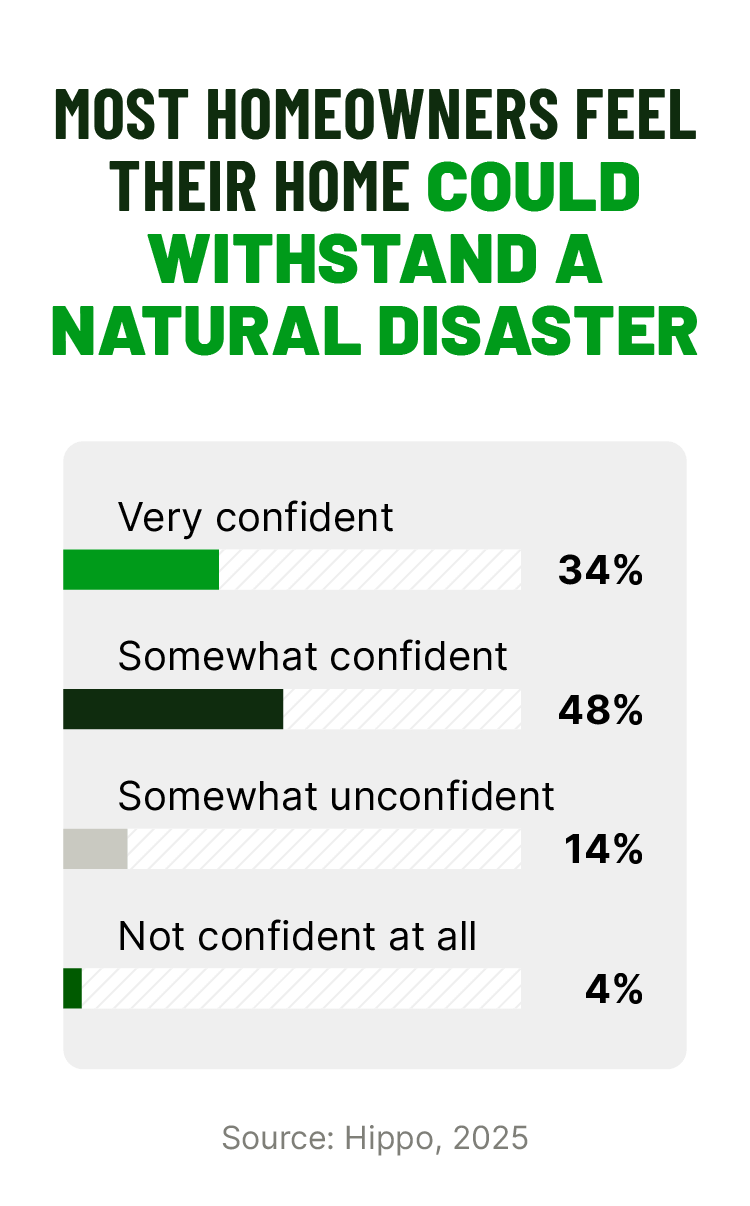

Overall, 82% of homeowners say they feel somewhat or very confident their home is prepared to withstand a natural disaster, according to our Disaster Preparedness Survey:

The West

The South

The Northeast

The Midwest

Extreme weather predictions for 2026

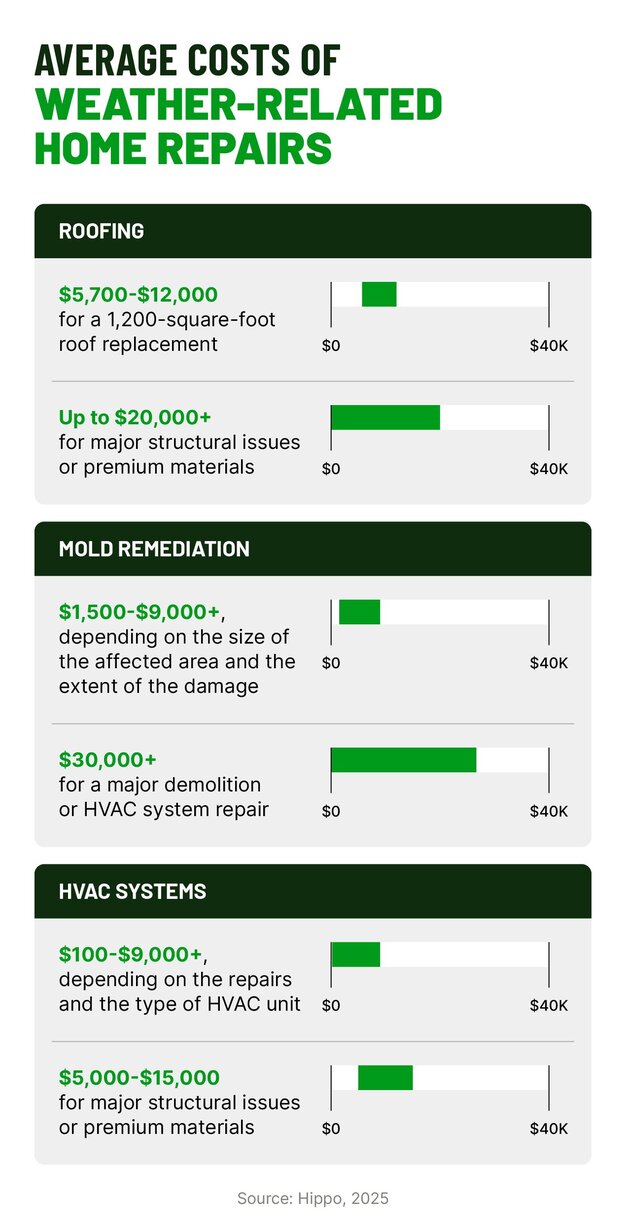

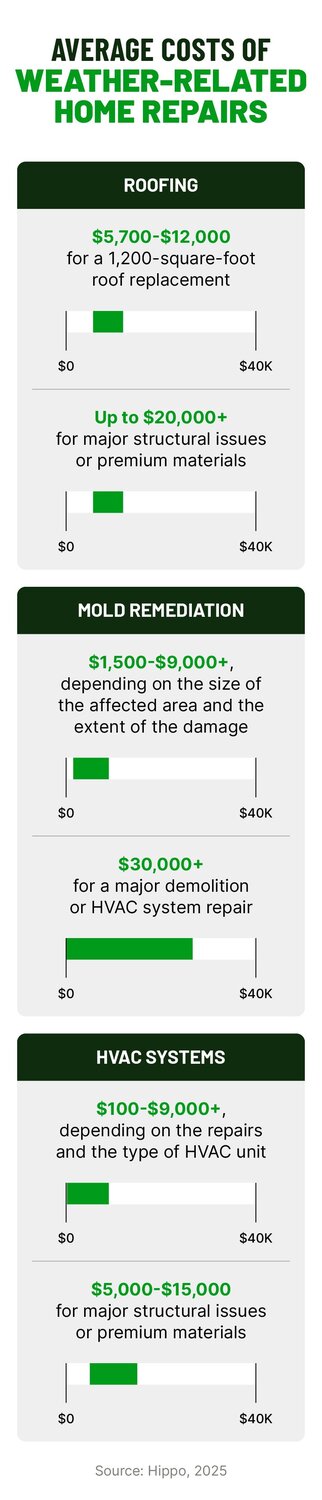

Nearly half of homeowners see unexpected repair costs rise more than $5,000

37% of homeowners repaired roof damage in 2024, making it one of the most common unexpected home repairs. Around 1 in 5 repaired water damage caused by flooding.

While you can’t prepare your house for every possible storm, taking small steps today could prevent costly repairs later down the road.

- Checking and cleaning gutters and downspouts to ensure proper drainage.

- Inspecting your roof, chimney, and attic for damage. Look for visible damage like missing or cracked shingles, or for signs of moisture, leaks, or mold.

- Keeping insurance and records up-to-date. Confirm coverage limits and check for specific add-ons, such as flood or earthquake insurance.

- Creating an up-to-date home inventory with photos and receipts. Store copies digitally as well as off-site.

Preparing your home for an upcoming storm

Hurricanes

- Board up your windows or close your storm shutters, if you have them.

- Use sandbags to prevent flooding around the foundation of your home.

- Tie down or tie together large outdoor furniture and move small outdoor items indoors.

- Stock up on non-perishable food, drinking water, and pet food. Fill your car with gas and stock up on gas for your generator, if you have one. Move your car to higher ground if you’re concerned about flooding.

- Charge your devices and make sure flashlights and other small electronics have new batteries.

- If you live in an area that might be evacuated during a storm, make an emergency preparedness plan. Pack a go bag with your vital documents, medications, clothing, cash, and other essentials, and decide where you will go in case of an evacuation.

Winter storms

- Stock up on emergency supplies, such as non-perishable food, prescription medicine, pet food, and first aid supplies.

- Check if you have a properly vented heat source, like a fireplace, wood stove, or space heater.

- Make sure your carbon monoxide detector is working properly.

- Gather extra blankets and clothes to keep at your home and in your car, including mittens, hats, boots, and coats.

Heat waves

- Weather-proof your home affordably by weather-stripping doors and windows, using window reflectors, or covering windows with shades.

- Spend time in cooler public spaces, like libraries or shopping malls, if you don’t have AC.

- Watch for signs of heat-related illnesses.11

Steps to take after extreme weather hits

- Carefully examine your home and property for hazards such as downed power lines or structural damage, like cracks or leaning walls. Don’t enter a building if you’re not sure it’s safe.

- Take note of any damage to your property, buildings, and belongings. Write down a detailed description and take photos and videos of the items and damages. Note the date and time, too.

- Contact a professional to conduct a more thorough investigation for structural damage, water damage, or other problems, if necessary.

- If any utilities aren’t visibly damaged or aren’t working properly, contact your provider and report it.

- Contact your insurance company and begin the claim process, if necessary. Keep thorough records and receipts when you get quotes from contractors.

Prepare for the unexpected with Hippo

External sources:

- NOAA. (2025) Billion-Dollar Weather and Climate Disasters

- Gallup. (2025, April) Extreme Weather Affects Sharply More in Western U.S.

- National Weather Service. (2024) Hurricane Milton Impacts to East Central Florida

- Houston Public Media. (2024, September) Coastal flooding is getting more common, even on sunny days

- NOAA. (2024, November) Hurricane Helen’s extreme rainfall and catastrophic inland flooding

- EPA. (n.d.) Climate Impacts in the Midwest

- U.S. Environmental Protection Agency (EPA). (2025, October) 2025 Southern California Wildfires

- NOAA. (2025, October) El Niño/Southern Oscillation (ENSO) Diagnostic Discussion

- NOAA. (2025) Three Month-Outlooks Official Forecasts Jul-Aug-Sep 2026

- NOAA. (2025) Three-Month Outlooks Official Forecasts Aug-Sep-Oct 2026

- U.S. Department of Homeland Security. (2025, July) Extreme Heat

Related articles

From Gutters to Foundations: How Cold Weather Weakens Homes

Building for the Future: How Residential Construction is Adapting to Weather and Climate Change

Burning Issue: 41% of Homeowners Surveyed Experience Heat-related Home Damage Due to Summer Weather

Can Your Homeowners Insurance Weather Hurricane Season?

The 9 Most Expensive Home Repairs to Watch Out for in 2025