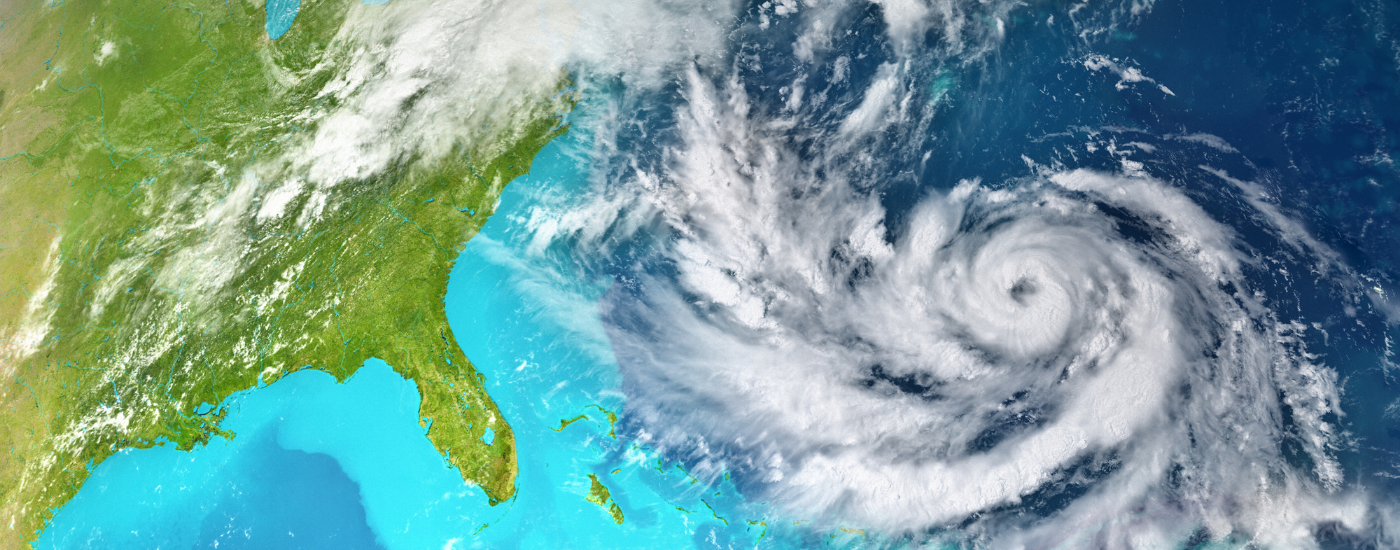

Hurricane season runs from the beginning of June through the end of November, with most hurricanes making landfall in August and September. And while hurricanes do form in the Pacific, the West Coast of the United States has never been struck by one. However, you can’t say the same for the Atlantic Coast. States like Florida, Texas, Louisiana and both Carolina’s are at the top of the list for Hurricane prone states, with Florida seeing almost twice as many landfalls as neighboring states.

You shouldn’t wait until a hurricane has almost arrived to ensure you have the right types of protection for your home. Insurers usually won’t allow homeowners to add the needed supplementary coverage to their policies if they are already under a hurricane watch.

It is vital to know your home’s risk of hurricane or tropical storm exposure and to review your homeowners insurance policy for any gaps. If you need supplemental insurance, make sure you do so well in advance of Hurricane Season and before the first storm warning.

Review your Policy

The good news is that most home insurance policies will automatically cover some of the damages incurred during a hurricane or tropical storm but not always. That is why it is so important to assess your coverage with as little bias as possible. If you live in a high-risk area prone to hurricanes or tropical storms, you may want to add wind damage to your current policy. Even with supplemental wind damage coverage, you may not have full protection from potentially devastating destruction caused by a hurricane. Again, planning ahead and having coverage before the wind starts to blow is key. Make sure you carry the necessary amount of coverage in a region susceptible to a natural disaster. You may have to shop around and see how other insurers cover your area against severe storm damage.

Your home insurance policy should never be ‘set it, and forget it,’ and your insurer should always want you to be proactively protected against any harm that may come to your home. Here at Hippo, we use advanced technology to frequently reassess your coverage to do our part in making sure you not only think about extra coverages you may need but also to streamline your policy and ensure you aren’t paying for coverages you don’t need.

Consider your coverage

After reviewing your policy with a fine-tooth comb, determine which types of coverages you may need to add to be fully protected in the event of a hurricane. You can click each coverage type to read a more detailed explanation in Hippo’s Learn Center.

-

Replacement Cost - pays you to repair or replace your home and belongings under covered perils

-

Flood Insurance - provides financial protection for your home’s structure and your personal property if damaged by floodwaters

-

Windstorm Insurance - protects your home, belongings, additional structures on your property from high wind damage

-

Water Backup Coverage - covers items and structures damaged from accidental water overflow

-

Loss of Use Coverage - provides financial assistance if your home becomes unlivable

-

Service Lines Coverage - protects you from having to pay for damage to your underground utility lines

-

Hurricane Deductibles - a separate deductible expressed as an extra percentage of your home’s insured value and property risk

Talk to an expert

Of course, buying online is easy, but when it comes to customizing something as crucial as a home insurance policy, it can make all the difference to talk to an expert in the industry. Doing your own research online is a great starting point, and once you have all the information you need, it’s time to meet with your insurance agent, who can answer any questions you may have or address any concerns. In addition, knowing and understanding what is and isn’t covered by your home insurance policy will make all of the difference if a hurricane makes landfall in your neighborhood.

Don’t have time to speak with one of our experts? Already have an idea of the coverage you need? We’ve got you covered. Get a quote online in 60 seconds or less.

Here at Hippo, we know that owning a home is a lot of responsibility, so we are here at your convenience, 24/7. The more you know, the more you will be able to get out of your homeowners insurance policy when you need it most.