Multigenerational homes: How families are hacking the housing market

Buying a home with extended or chosen family can be rewarding, but it also comes with its own unique set of challenges. Today, nearly 1 in 6 homebuyers are in multigenerational households.1

Our deep dive into multigenerational living looks at who’s buying a house with family, why they’re choosing to live together, and how their insurance needs might change with more family members under one roof.

Key takeaways

- 67% of people in multigenerational households cite financial reasons for their living situation.

2Pooling resources can make homeownership more realistic–it takes at least two working adults each earning $74,480 per year to afford the average U.S. home worth $357,445.3,4 - Multigenerational living can help aging family members stay on top of home maintenance and protection, like keeping insurance documents up-to-date. According to the 2026 Hippo Housepower Report, 42% of baby boomers have either never attempted DIY home maintenance or often encountered problems or regrets when they did.

- A mortgage is a major expense, but it’s one you can plan for. What catches homeowners off guard tends to be other costs: 76% of homeowners say other home expenses, like utility bills or surprise repairs affects their financial stability. Having family members to share that load can make a difference.

What is a multigenerational home?

A multigenerational household typically consists of an adult, aged 18 or older, living with other adult relatives who are not their spouse or partner—parents, grandparents, aunts, uncles, or other extended family members.

These households often need homes with additional square footage: more bedrooms, flexible spaces, or separate quarters altogether. Properties with accessory dwelling units (ADUs), finished basements, or granny flats, tend to be popular.

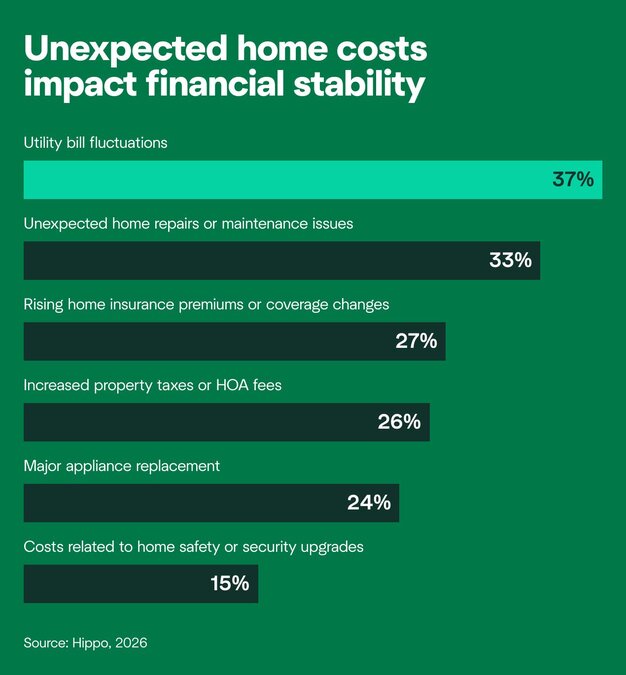

While multigenerational living was common in the U.S. before the 20th century, today’s high cost of living has driven its resurgence.5,6 Financial reasons are cited by 67% of those in multigenerational households, and it’s easy to see why. According to the 2026 Housepower Report, utility bill fluctuations (37%), unexpected home repairs or maintenance issues (33%), and rising home insurance premiums (27%) all impact financial stability. When those costs are shared, the whole household feels more stable.

![Graphic showing the top home-related expenses impacting financial stability. 37% of homeowners cite utility bill fluctuations, more than any other expense.]](https://cdn.builder.io/api/v1/image/assets%2F87a865fc472c4b69863d5e7f8aa60d5c%2Ffe78edf359db48d1a0e6101592078e91?width=919)

How a generational home impacts your insurance

Multigenerational living doesn’t just shape the kind of home you buy—it also affects your home insurance. If you’re in a multigenerational household, there are a few coverage areas worth reviewing with your licensed insurance producer:

- Adding additional personal property coverage. Many standard home insurance policies cover basic personal belongings, but they don’t cover everything. Scheduled personal property coverage can help protect valuable family heirlooms, expensive technology, or other high-value items brought into the home.

- Adding family members to your policy. If people living in your home aren’t listed on your current policy, an additional insured endorsement extends your liability coverage to anyone who lives in or has a financial interest in your home.

- Updating your insurance terms. If you remodel or add space to accommodate family members, consider reviewing your current policy to see if it’s time for an update.

Benefits of multigenerational living

Multigenerational living isn’t for everyone. But, for many families, it offers meaningful advantages across these areas.

Caregiving help

Americans are aging. The share of people 65 and older grew from 12% in 2004 to 18% in 2024, now outpacing the share of children.7 As elder care becomes a growing reality for more families, multigenerational households offer a built-in solution: older adults can receive support from family members, reducing the need for hired care or assisted living, while grandparents and other relatives can contribute to child care.

People with disabilities or chronic illnesses may also benefit from living with family members who can provide daily support. These arrangements are especially common among lower-income households, defined by the Pew Research Center as households making less than $42,000 annually. More than half (51%) of people in this group say they're either caring for an adult family member or receiving care themselves. Another 32% say they're providing or receiving help with child care.8

Cultural reasons

For many families, living together across generations isn’t a financial decision, it’s a reflection of values. Asian, Hispanic, and Black families, in particular, are driving the rise of multigenerational living in the U.S. More than 1 in 4 (28%) adults in these households say the main reason is that it’s the arrangement they’ve always had.8

This often overlaps with caregiving, as some cultures prioritize keeping relatives together at home rather than seeking outside support. Living together is seen as both a family responsibility and source of connection.

Affordability

Multigenerational households report similar incomes to other homebuyers. In 2024, the median household income was $109,300 for multigenerational buyers compared to $109,000 for all homebuyers. What this suggests is that individuals who might face financial constraints on their own are pooling resources to achieve what could otherwise be out of reach.

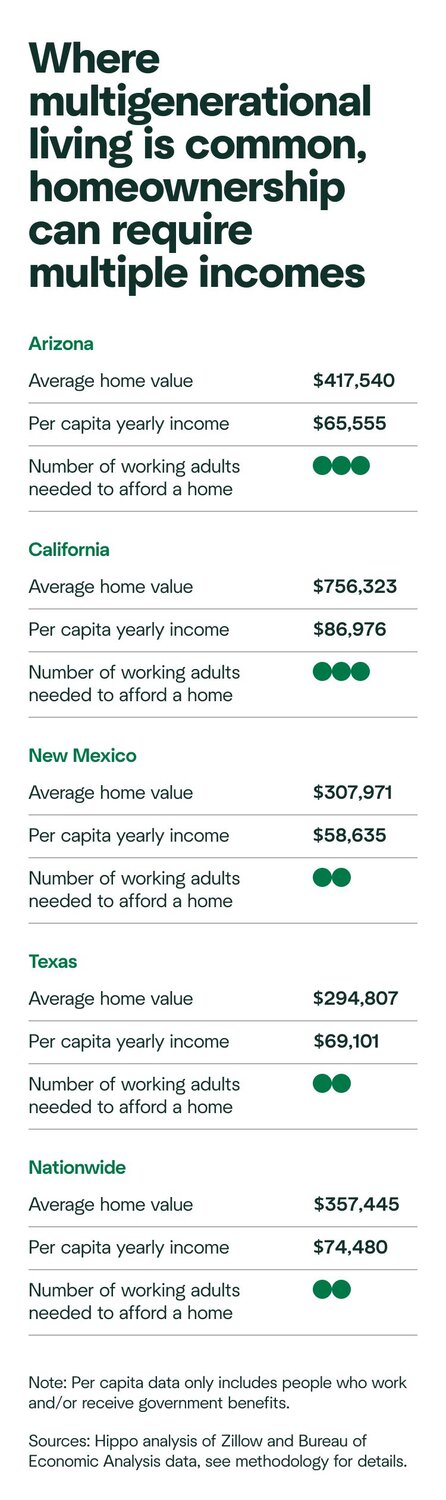

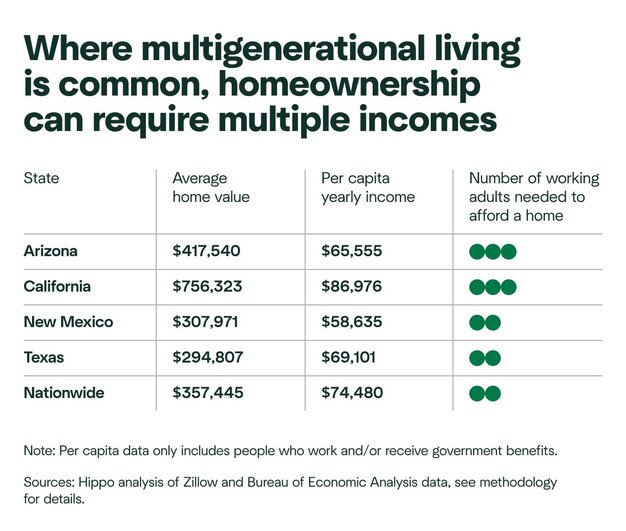

This is most visible in states with high rates of multigenerational living, like California, Arizona, New Mexico, and Texas. Many of these states have notoriously high home prices (like California) or lower-than-average wages (like New Mexico and Texas).3,4,9

In these markets, having multiple family members contribute to housing costs can make the difference between renting and owning.

Typically, a couple can afford a home if both people earn at least an average salary. According to a Hippo Insurance Services analysis of Zillow and Bureau of Economic Analysis data, it takes at least two people, each earning the U.S. per capita salary of around $74,480 per year, to afford the sale price of the average home. (A home is considered affordable if its final sale price is around three times someone's yearly salary.)

But if someone makes less than $74,000 per year, or they're a single-earner household, they may need more family members at home to contribute to the mortgage. In some states where multigenerational homes are common, like California and Arizona, it takes at least three people.3,4

Overall, Americans in multigenerational households are less likely to live in poverty. Most say it’s been a positive experience, with at least half describing it as convenient and rewarding.9

Challenges of multigenerational living

The benefits are real, but so are the tradeoffs. More than 1 in 4 (26%) people in multigenerational households have privacy concerns, and 20% point to differences of opinions and beliefs as a key frustration.10

Space can be another limiting factor: 28% say there isn’t enough space to live comfortably. That rises to 38% in lower-income households.2

Multigenerational living doesn't always translate to lower housing costs. If you're the primary earner supporting aging relatives or adult children who can’t yet contribute financially, you may still shoulder the responsibility. More than 1 in 3 (35%) people ages 40 and older who live with a parent pay their entire rent or mortgage themselves.2

It’s also worth factoring in the practical reality of more people in the home. Additional wear and tear can lead to higher repair and insurance costs over time.

Find the insurance policy for your family home with Hippo Insurance Services

Whether you're considering it or already living in a multigenerational household, it’s important to discuss finances, house rules, and long-term plans before making the leap. If you do decide that multigenerational living is right for your situation, make sure your home insurance adequately covers all residents and reflects the full value of what you’ve built together.

Not sure where to start? Your dedicated Hippo producer can educate your entire household—no matter how big it is—on the right insurance options for your situation.

Survey Methodology

The 2026 Housepower Survey was completed on September 22, 2025, and conducted by Centiment on behalf of Hippo. The results are based on 1,619 completed surveys. In order to qualify, respondents were screened to be residents of the United States, over 18 years of age, and own a home. Data is census-balanced, and the margin of error is approximately ±2% for the overall sample with a 95% confidence level.

The MOE and confidence level for data filtered by specific demographics (subgroups) may differ from the overall result. Because these subgroups are naturally smaller than the total sample, they may have a larger margin of error than the ±2% for the full data set.

Data analysis methodology

To determine the number of working adults needed to afford a home, Hippo analyzed the average home values from the Zillow Home Values Index and per capita personal income from the U.S. Bureau of Economic Analysis' Personal Income by State resource.

Average home values are Zillow’s January 2025 “Zestimates” of a home’s market value, which incorporates public, MLS, and user-submitted data. Per capita personal income is the income received by people living in each state and Washington, D.C., from wages, proprietors' income, dividends, interest, rents, and government benefits.

For this analysis, an affordable home is defined as a house that is priced at three times the area’s per capita income. Hippo compared the difference in price between an area’s affordable home value, adjusted for inflation, and its actual average home value, then rounded to the next whole number.

External sources

- National Association of Realtors (NAR). (2025) Making Extra Room at the Table: Multi-Generational Homes in the United States

- Pew Research Center. (2022) The experiences of adults in multigenerational households

- Zillow. (2026) United States Housing Market

- Federal Reserve Bank of St. Louis. (2026) Personal income per capita

- National Library of Medicine. (2011) The Decline of Intergenerational Coresidence in the United States, 1850 to 2000

- CNN. (2026) Inflation remained at 2.7% in December, as high prices continue to weigh on many Americans

- U.S. Census Bureau. (2025) Older Adults Outnumber Children in 11 States and Nearly Half of U.S. Counties

- Pew Research Center. (2022) Financial Issues Top the List of Reasons U.S. Adults Live in Multigenerational Homes

- U.S. Census Bureau. (2023) In 2020, 7.2% of U.S. Family Households Were Multigenerational

- Rocket Mortgage. (2024) Multigenerational homes: What it's like living in one

This article is for informational purposes only. The content reflects general homeowner considerations and is not professional advice. It also includes observed trends within the surveyed population and certain additional information compiled from sources not affiliated with Hippo. While we believe this information to be reliable, we do not guarantee its accuracy or completeness. For any insurance-related decision, please consult your licensed insurance producer.

Sources cited are publicly available and referenced in February 2026.

Related Articles

Critical Home Maintenance Upgrades: 5 Best ROI Home Improvements in 2024

Report: Where Homeowners Turn for Maintenance Advice in 2024

Hippo Housepower Report: Homeowners Gain Ground, Face New Challenges in 2026

State of Suburbia: Where Suburban Development is Surging

AI adoption study: The growing generational divide in home insurance