15 Ways To Afford Your Dream House

Anyone who has watched an HGTV show might picture themselves going on tours to find their own dream home. Actually doing so might seem like a pipe dream.

But with new opportunities to save for a home and less strict down payment requirements, buying a home is a realistic goal for many households. So when you’re ready to stop imagining yourself on an episode of House Hunters and start your own search, we’ve put together a guide on how to afford a house.

How much house can I afford?

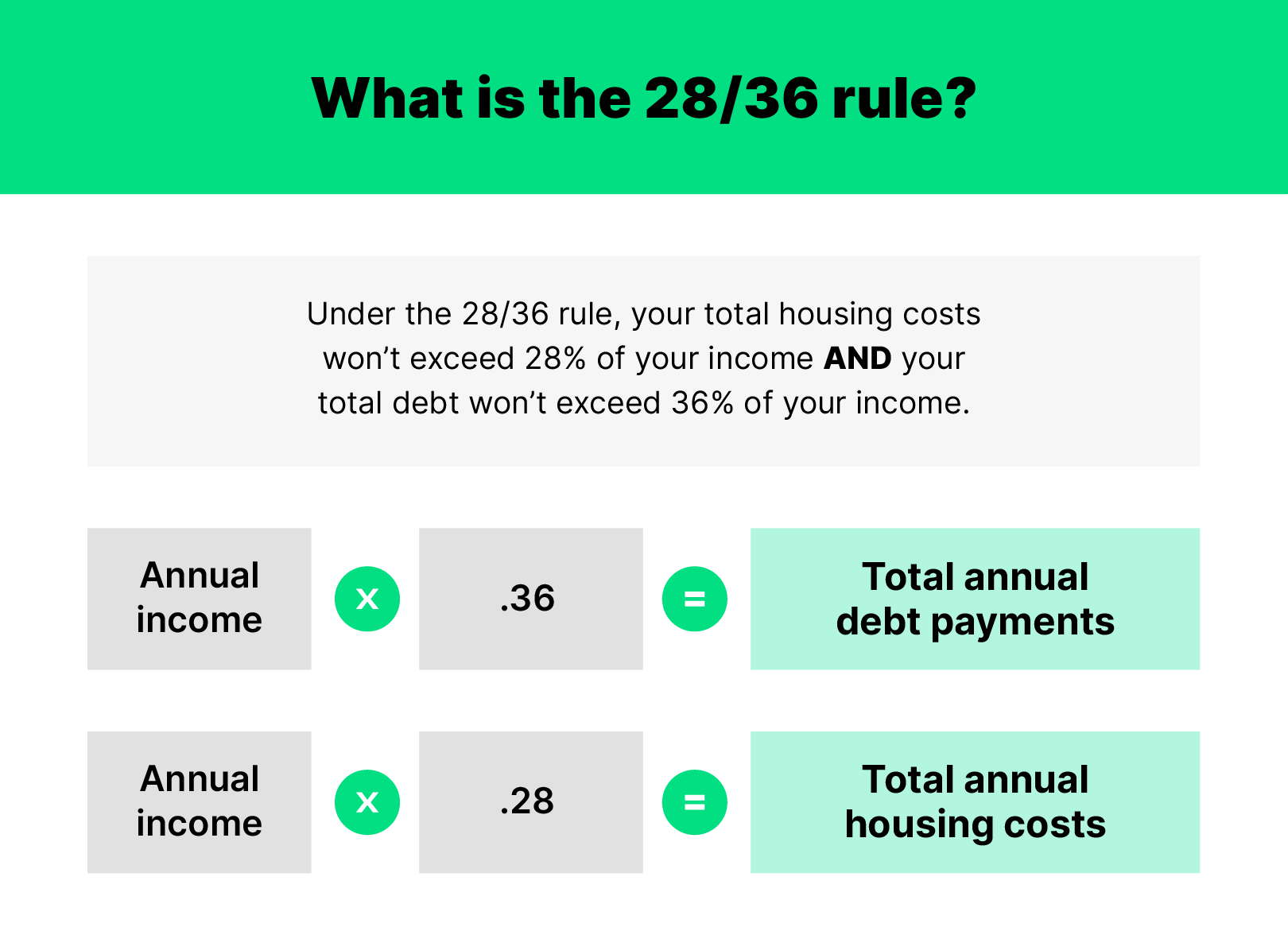

When calculating how much home to look for, people often refer to the 28/36 rule. With this rule, your housing expenses shouldn’t exceed 28% of your annual income and your total debt shouldn’t exceed 36% of your annual income.

If that seems confusing, let’s put it into a real-life perspective. Say you earn $55,000 per year, or $4,583 per month. Using the 28/36 rule, that would mean you would want to keep your total monthly debt payments below 36% of your income, or $1,650. You also want to keep your total monthly housing expenses below $1,283, or 28%.

However, this doesn’t mean you can afford a $1,283 monthly mortgage payment. Let’s say your car loan, student loan and credit card payments total $650 per month. In order to keep your total payments below $1,650, you’ll likely need to keep your monthly housing expenses below $1,000.

How to afford and save for a house

Financing a home can seem like a lofty goal. But being smart with your finances can help you put it into perspective.

1. Look into loan or financing options

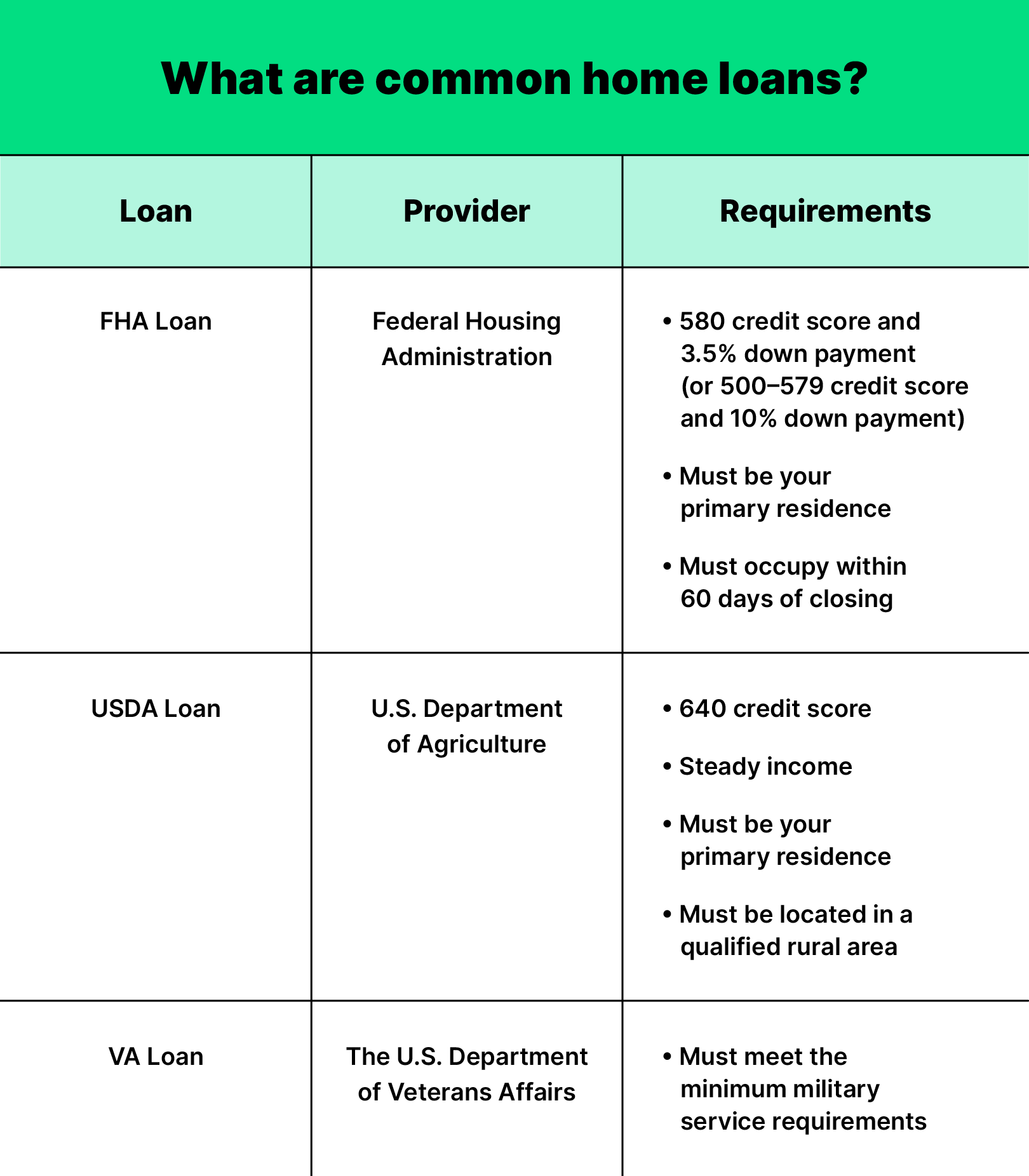

Homebuyers, especially first-time homebuyers, have loan options that can help them put a down payment on their dream home. A few common loan options are:

- FHA Loans: The Federal Housing Administration (FHA) aims to help people with lower credit achieve homeownership. In addition to a lower credit score for qualification, the FHA also aims to offer lower down payments and closing costs.

- USDA Loans: The United States Department of Agriculture (USDA) will provide no-down-payment mortgages to eligible buyers looking for a rural home.

- VA Loans: For military members seeking homeownership, the U.S. Department of Veterans Affairs (VA) provides loans to veterans and active-duty servicemembers.

2. Pay down your existing debts

Existing debts can make the home buying process more difficult for potential homeowners. Lenders might be less likely to provide a mortgage to someone with a low credit score or a high debt-to-income ratio. What’s more, those with more debt who obtain approval for a loan will most likely have a higher interest rate. Neither of these scenarios may be ideal for a homebuyer.

When you first decide to buy a home, you’ll likely want to look at your debt and work on paying it down before making more concrete steps like getting preapproved or getting ready to put in an offer on that dream house.

3. Tap into your retirement savings

If you’ve been paying into your retirement fund, you may be able to tap into that money for your down payment. You can borrow half of your invested amount or $50,000, whichever total is less. If you choose to take from your 401(k), it’s imperative to keep in mind that this will help you pay your down payment, but you’ll incur an early withdrawal penalty if you’re under 60 and still employed. You’ll also likely have to pay back into your 401(k) to make sure you’re still set up to retire.

4. Buy a fixer-upper

More than just an HGTV fad, fixer-upper homes can help people achieve their dream of homeownership. Fixer-uppers can often have a lower price tag than modern, finished homes. If you are DIY-savvy or just willing to put in the work, purchasing a fixer-upper may get you signing a deed without breaking the bank.

5. Budget accordingly

While you are most likely familiar with the idea of having to save for the down payment and mortgages, there are many hidden costs associated with home buying that might sneak up on you. When looking at your household budget, determine where you can cut back to set aside money for the home buying process. You may also want to set up a dedicated contribution to your home savings that will become a fixed part of your budget while you’re saving up. Setting aside money specifically for ongoing home maintenance can help you keep up with your home's needs.

6. Determine how much house you need

It can be tempting to splurge on the home with a three-car garage, a movie room and a few extra bedrooms. But unless you’re frequently hosting your extended family, you most likely don’t need to have so much house. Not only is it more to clean and maintain, but it’ll also be more expensive to pay for. Think critically about how much square footage you will realistically use and can afford when you start shopping.

7. Start side hustling

A temporary side hustle can help pad your bank account without taking up too much of your time. While you’re in the process of saving, consider starting up a side hustle to save for your down payment. You can perform services like dog walking, babysitting or food delivery. Depending on your skill set, you can also take on freelance work like copy editing, photography or making crafts to sell on an online marketplace.

8. Cut out some luxuries

Americans spend an estimated $660 per month on dining out. That could translate to about $8,000 per year. If you’re looking to put a 20% down payment on a $300,000 home, you’re paying about 13% of the down payment just to eat out. When saving money, it’s important to look for these types of expenses and identify ways to cut down on unnecessary spending.

While you don’t have to cut luxuries like eating out, going to a spa or buying expensive clothes completely out of your budget, you may want to consider cutting down on that spending while you’re trying to buy a home.

9. Try house hacking

House hacking means buying a home and renting out parts of it that you aren’t occupying. This could mean anything from letting a tenant live in the guest bedroom to converting the garage into an apartment. The logic behind house hacking is that you can buy the home and then take on a tenant to pay a good portion of the mortgage payments. House hacking is most commonly seen in expensive markets where mortgage payments might be high.

10. Get prequalified or preapproved

Getting prequalified or preapproved for your home can give you exact insight into what you can afford. You’ll get preapproved for a certain amount and can tailor your home search to that amount. A preapproval can help make sure you’re only looking at houses that are in your price range so you can start moving forward as soon as you fall in love with one.

11. Look into rent-to-own

If you’ve ever heard of leasing a car before you purchase it, you can apply the same philosophy to buying a home. Some leases will allow you to rent the home for a bit before you commit to purchasing it. In some cases, the rent you pay throughout your lease period will be applied to the home’s cost and can help reduce your down payment or mortgage when you do decide to make the purchase.

Before jumping into a lease-to-own agreement, you’ll want to consider the terms and assess the risks. For one, you might end up paying more in rent than you would on a mortgage. And depending on how much of that your landlord puts toward your home purchase, it may not actually result in high down payment savings. (For example: if you pay $2,500 in rent and your landlord agrees to put $200 of that per month toward the down payment, that’s only $12,000 at the end of five years).

12. Move to a state with low property taxes

Part of your property taxes will likely be due at closing and will add to the amount that you need to pay before you can secure your new home. Moving to a state with lower property tax rates (like Texas, Hawaii, Alabama or Louisiana) can help you save some of this money. You can also negotiate with your seller while drawing up your contract to have them cover some or all of the property taxes that are due at close.

13. Get ready to negotiate

There are many hidden costs that might pop up throughout the home buying process. To help reduce some of that burden, you should be ready to negotiate for the seller to take care of some of those closing costs. You can negotiate to have the seller pay for a portion of the property taxes, inspection, repairs or other costs. That way, you can focus solely on paying your down payment and mortgage.

14. Look into a rebate

A rebate is when the buyer’s agent gives the buyer a portion of their down payment back after the deal has been made. Usually, the agent will give the buyer a portion of their commission. Most states in the United States will allow agents to give their clients a rebate when they buy a home. If this interests you, look into whether your state allows homebuyer rebates and negotiate one with your agent ahead of time.

15. Look at surrounding areas

City living is an admirable goal, but homes in urban areas often come with a high price tag. Looking beyond city limits to neighboring suburbs and smaller cities can get you close enough to pop into town for a meal or some sightseeing but far enough away that you’ll be able to afford a bigger home.

For example: The median cost of a home in San Francisco is $1.3 million. If you travel eight miles and 25 minutes away to Oakland, you’ll find a median home cost of $749,000.

How much should you put down on a house?

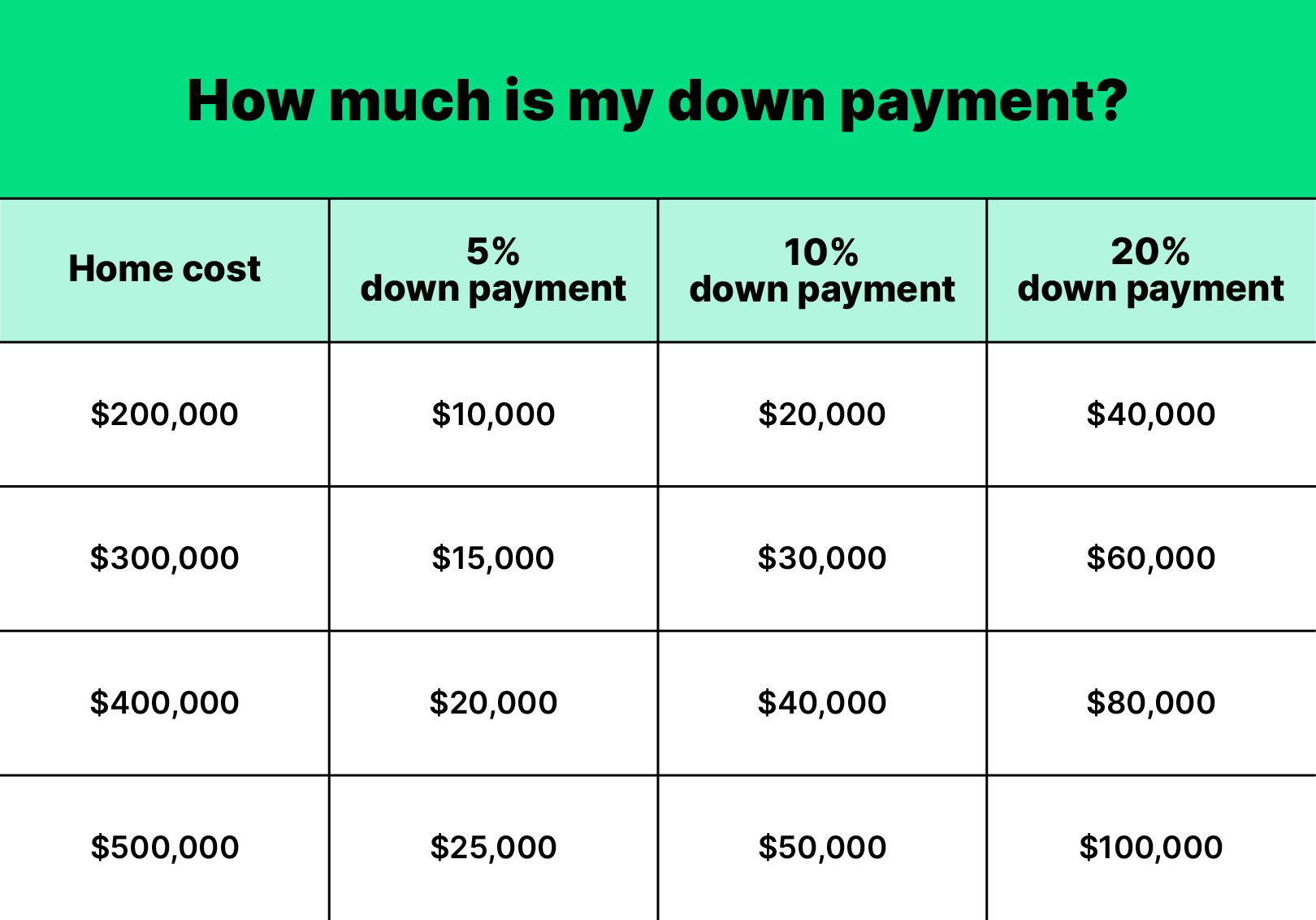

There once was a time when a 20% down payment was the expectation, but many people don’t/can’t shell out quite so much to secure a home. In 2018, the average down payment was somewhere between 5 and 6% of the home’s cost.

The median home cost in the U.S. is $374,900. If you were to put down 6% on that home, your down payment would be $18,745, as opposed to the almost $75,000 down payment that would come with putting 20% down on that home. A $19,000 investment seems like a much more realistic goal.

There are many ways to afford a home. And though there are many ways to protect your investment, here at Hippo we are committed to providing home buyers with the confidence they need every step of the way.

Contact us for homeowners insurance to see how we can help you along your home buying journey.