How Long Does a Mortgage Pre-Approval Last?

A mortgage pre-approval will last for somewhere between one to three months. As it takes an average of four and a half months to find your perfect new home, you shouldn’t apply for pre-approval until you’re ready to hunker down and start seriously shopping.

On the other hand, you don’t want to fall in love with your dream home only to lose out because your finances weren’t in order and another buyer swooped in. Getting your mortgage pre-approval will help instill confidence in the home’s seller that you’re a serious candidate while expediting the process of putting an offer in and closing on your home.

To help first-time and seasoned home buyers alike, navigate the pre-approval process, we’ve put together this guide to applying.

Key takeaways:

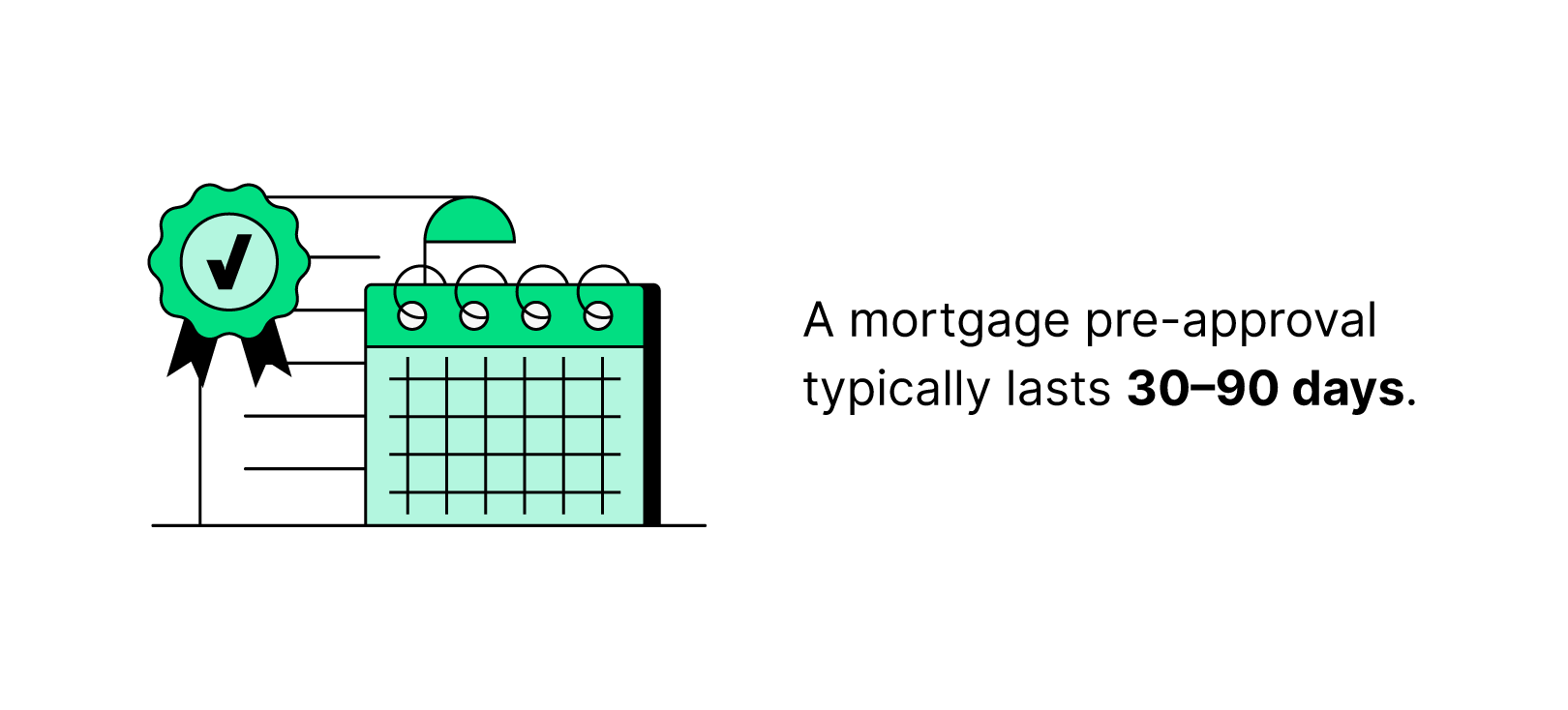

- A pre-approval will last between 30 and 90 days.

- Pre-approval requires a hard check into your credit.

What is a mortgage pre-approval?

A preapproval is exactly what it sounds like: an advanced approval of how much and what type of home loan you qualify for. Your chosen lender will evaluate your finances and write you a pre-approval letter to show to real estate agents and home sellers, proving you’re a serious buyer and showcasing how much you can borrow towards a home.

Why do you need a pre-approval letter?

Confidence is key — and sometimes, it gets you the keys to your new home. A pre-approval letter will help your agent and the home seller be confident in your intent and ability to purchase a home.

Beyond proving that you’re serious about your house hunting, a pre-approval letter will provide the following benefits:

- You can put in an offer as soon as you fall in love with a home

- You can focus on shopping for homes in your price range

- Sellers are more likely to pick your application

- Speeds up the home buying process to get you signing papers and packing boxes

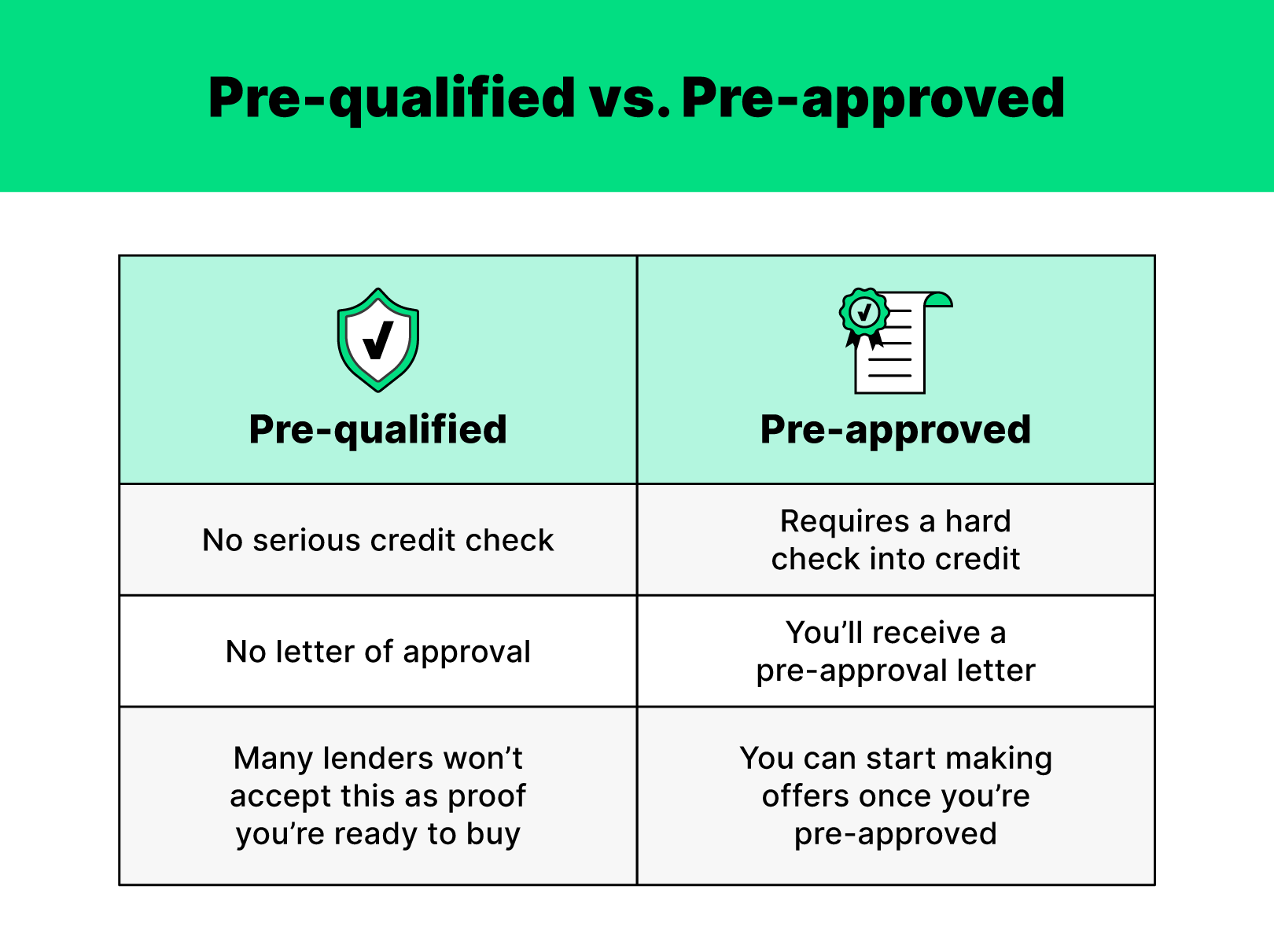

Pre-qualified vs. pre-approved: What's the difference?

Think of it this way: Getting pre-qualified is like going to sports practice and getting pre-approved is like playing in a stadium full of fans. Both involve the same basic activity, yet with pre-approval, the stakes are higher. Those who are more serious and prepared to buy a home should get pre-approved, while those who are still practicing or exploring their options can seek pre-qualification.

Pre-qualification requires a very basic overview of your finances to determine what you may be able to borrow. Typically, there won’t be a serious inquiry into your credit and your lender will use basic information to determine what your loan might look like.

Pre-approval, on the other hand, is the first serious step to home buying. You’ll need to submit sensitive data and authorize a hard check into your credit in order to get pre-approved, and lenders will typically use this information as a signal that you’re ready to buy.

How long does a pre-approval last?

Most mortgage pre-approvals will last up to 90 days, but some are valid for as little as 30 days. This is because your finances — including credit scores, bank statements and salary — can change rapidly and lenders will want to be sure that their investment in your home is protected. After about three months, they’ll want to reassess your financial reports for any changes that might impact the amount you can borrow.

How far in advance should you apply for pre-approval?

Purchasing home insurance, sending in an application to buy, closing on a mortgage — the timeline of the home buying process can be confusing. The pre-approval sweet spot is right after you decide you want to buy a home and just before you begin touring. Don’t apply before you get serious about home buying, but don’t wait until after you’ve found your dream home to apply for a pre-approval.

Your pre-approval will help guide you to houses you can afford and instill confidence in the seller that you want to buy. Thus, you should attend your first showing with a pre-approval ready to go in the event you fall in love and want to put in an offer. However, getting pre-approved before you’re ready to start touring and putting in offers might mean that it expires before you find the one.

What to do if a pre-approval expires

If three months come and go before you know it, don’t be too hard on yourself. Getting another pre-approval is as easy as contacting your lender and asking them to rerun your finances. Since your lender already has your information on file, getting re-approved shouldn’t take too much time.

How to get pre-approved for a home loan

While purchasing a home might seem like a big, daunting task, getting pre-approved for one is relatively simple. You’ll most likely follow these steps to get approved:

- Check your credit score. Before starting the pre-approval process, access your free credit score to gauge how good your credit is. If your credit score is below 620, you might want to take some time to improve your score before applying.

- Find a lender. Shop around with multiple mortgage lenders to find one whose terms and service fit your current needs.

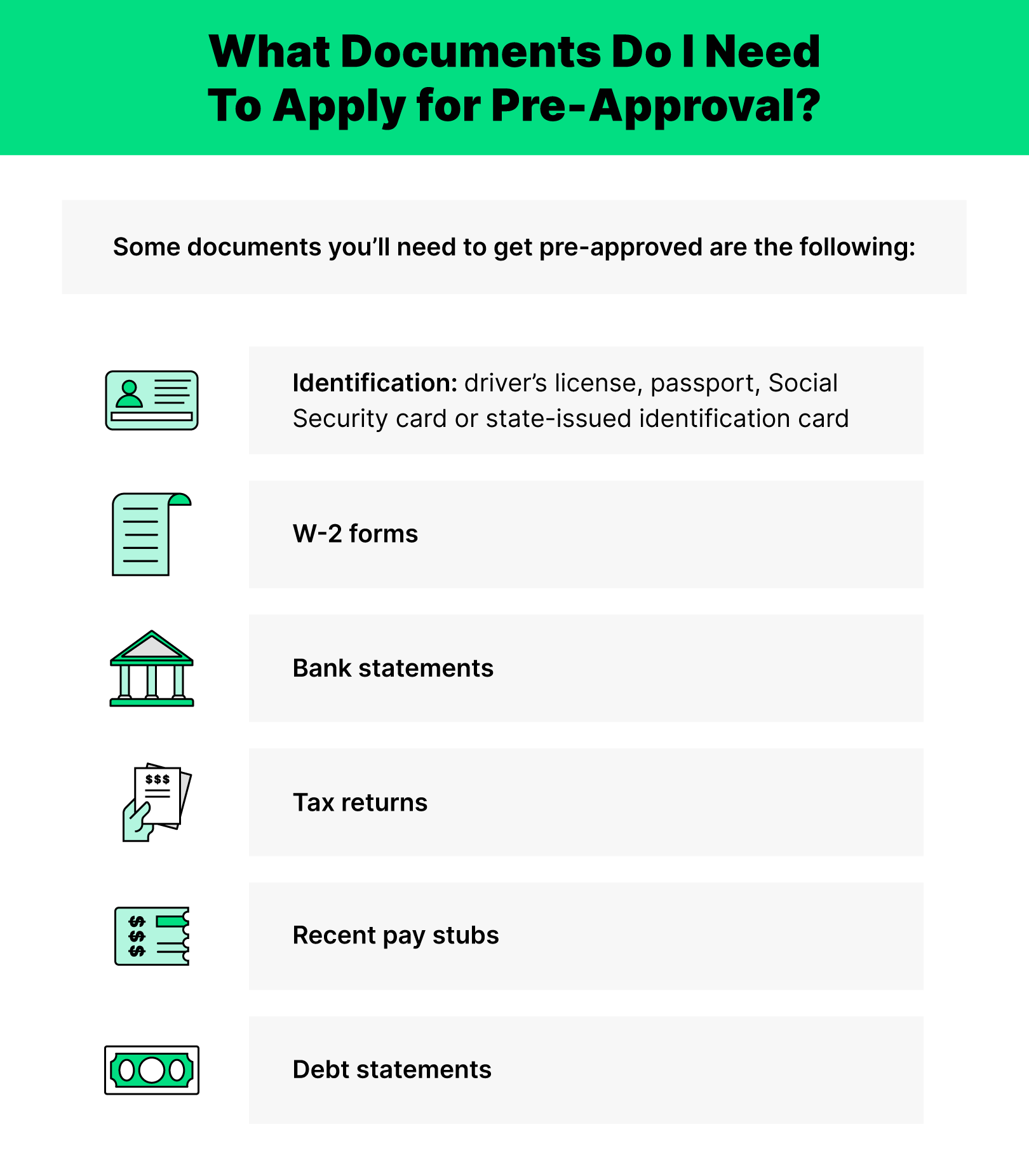

- Submit your documents. You’ll need to submit financial documents like a W-2, recent pay stubs, bank statements and tax returns to give your lender an overview of your financial health.

- Wait. Once your forms are submitted, wait for your lender to reach out to you with your approval letter.

How long does it take to get a mortgage pre-approval?

Depending on your chosen lender, a pre-approval could take anywhere from one to 10 business days. To prepare accordingly, you should start the pre-approval process about one to two weeks before your first house showing to make sure you’re good to go by the time your appointment date comes around.

Does pre-approval cost money?

Pre-approval is typically free, though some lenders may charge an admin fee for the time they spend running your financial reports and getting your letter together. If you want to avoid paying a fee to get pre-approved, another lender will typically complete the process for free.

Do pre-approvals hurt your credit score?

Obtaining a mortgage pre-approval means a hard check into your credit. Though it isn’t a loan application, the process is similar and may still reduce your credit score by a few points like any other inquiry into your finances.

To avoid unnecessary inquiries into your credit and further reductions in your score, don’t let your pre-approval expire and only apply when you’re getting serious about purchasing a home.

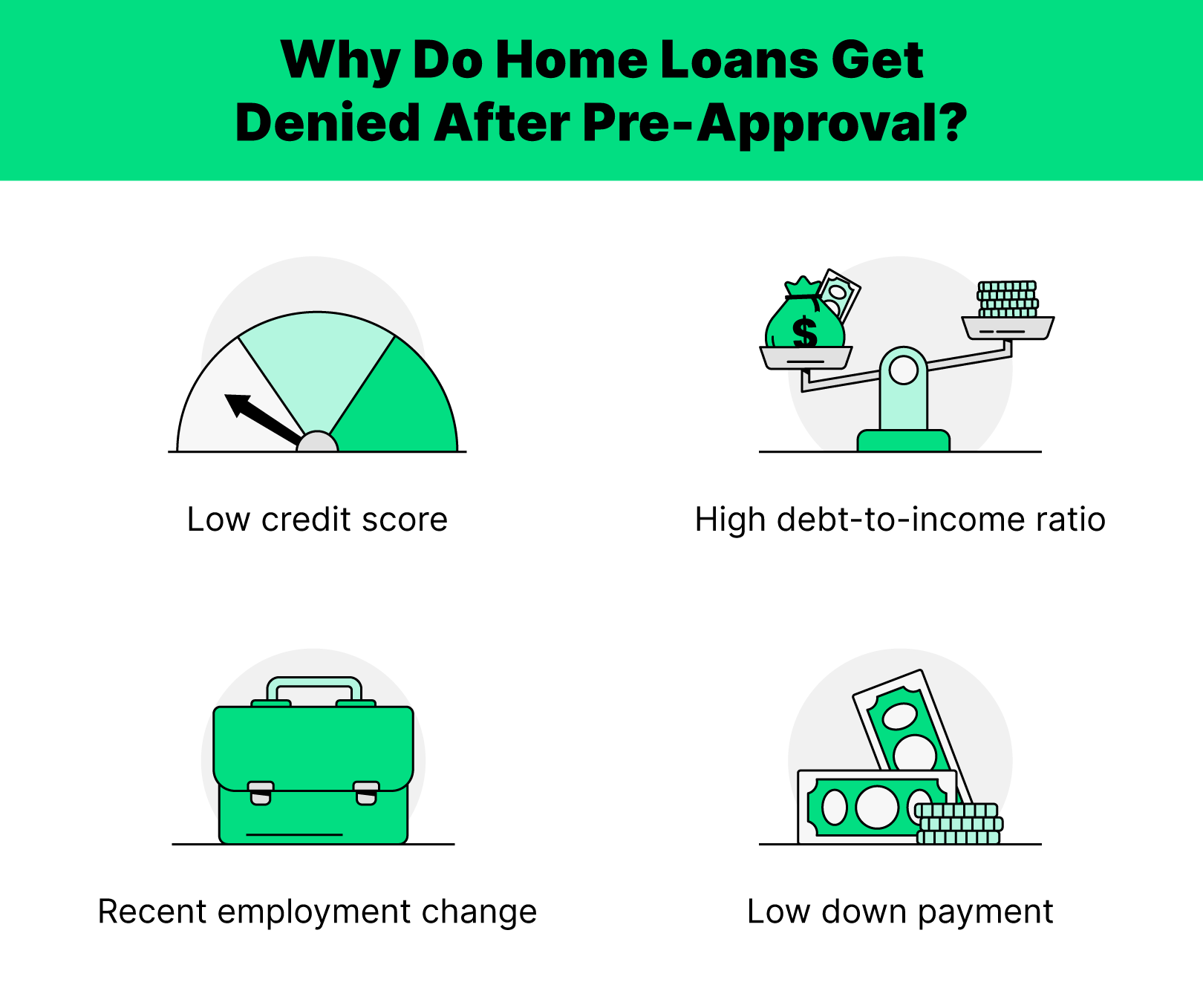

How likely is it to be denied a mortgage after pre-approval?

Getting denied for a mortgage can be heartbreaking — but, luckily, it’s an unlikely scenario. Only about 8% of home loan applicants get denied.

There are many reasons why a loan application could be denied, but the most common according to HSH are:

- Low credit score

- High debt-to-income ratio

- Recent employment change

- Low down payment

To make sure you stay approved after your initial application, avoid making large purchases, opening a new credit account or changing jobs. Keeping your financial information as steady as possible will show you’re a serious and reliable buyer.

Home buying is a serious process that can take months to complete. At the end of the road, you’ll want your new investment that you worked so hard for to be protected. That’s when it’s time to look for home insurance. Contact Hippo for a quick and easy home insurance quote that can get you on the road to confident homeownership — no pre-approval needed.