What is a deductible?

When it comes to insurance, the word deductible comes up a lot. But what exactly does it mean? Your deductible is the amount that you (the policyholder) agree to pay out of pocket before your insurance kicks in. The deductible would be subtracted (aka deducted) from your claim payment.

Do you have to pay a deductible upfront?

When filing a claim, your deductible is the amount you will be required to pay upfront before your insurance provider will provide financial assistance.

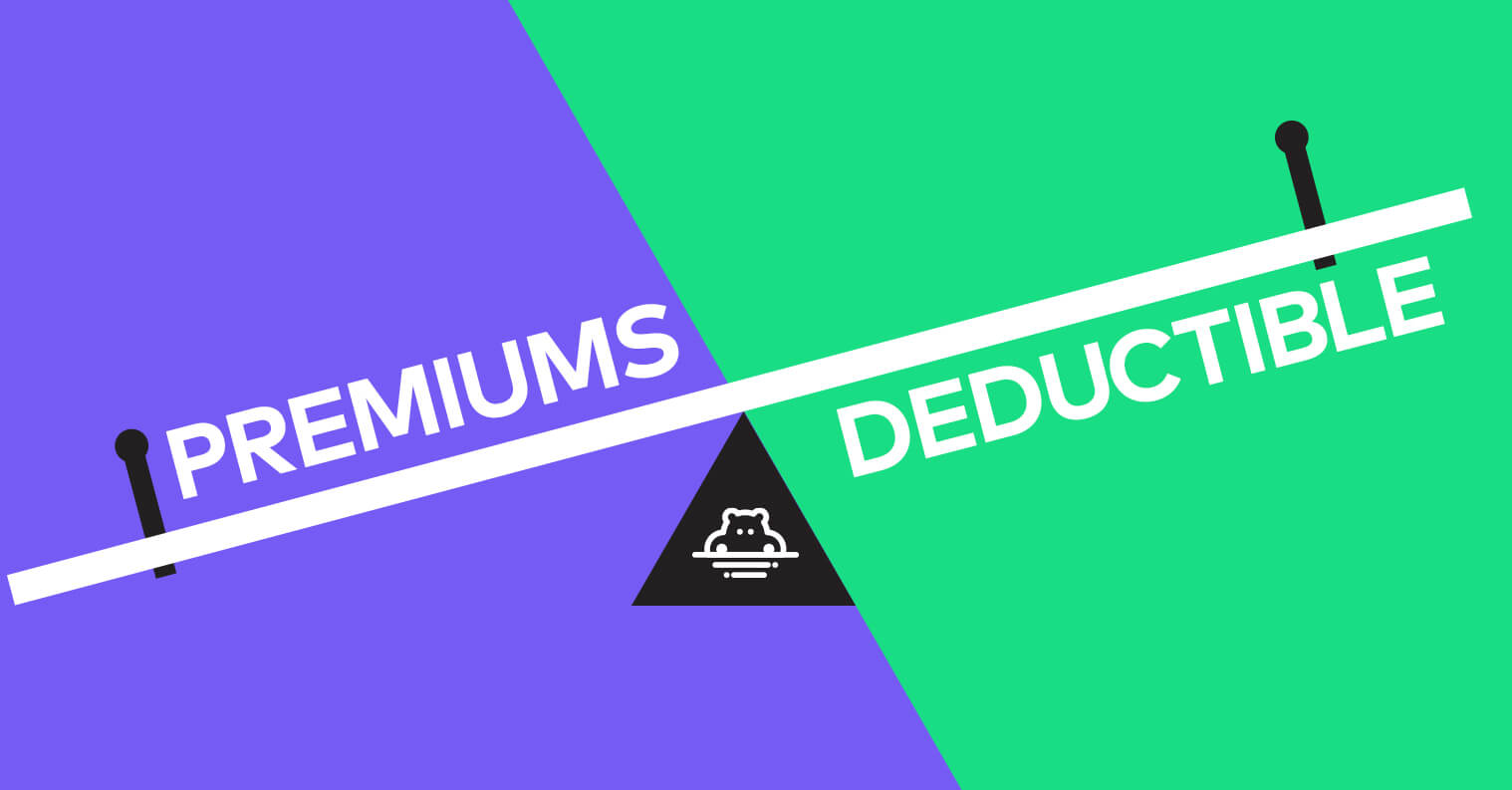

Financial experts often recommend increasing your deductible in order to reduce your monthly insurance costs. In general, it’s true that higher deductibles mean lower premiums. Some homeowners have saved thousands of dollars over time by bumping up their deductible. There’s something else to consider, though: Lower deductibles mean you’ll have lower expenses in the event that you have to file a claim.

Lower deductibles mean you’ll have lower expenses in the event that you have to file a claim.CLICK TO TWEET

Deductibles vs. Premiums

Most insurance policies have deductibles and premiums, but a deductible isn’t an amount you pay your provider like a premium. Another big difference? You select the amount depending on the options available. The insurance company still decides on what deductible amounts the customer is able to choose from.

Choosing the right deductible amount can feel like a balancing act. You’ll have to consider a few factors, like your financial resources, risk tolerance and how many claims you’re likely to file before your policy expires.

Are you financially prepared for the worst?

Your financial situation will probably play the largest role in your decision to opt for a low or high deductible. Essentially, you’re trying to figure out what you can afford in the short term and compare that to what you might…CLICK TO TWEET

Your financial situation will probably play the largest role in your decision to opt for a low or high deductible. Essentially, you’re trying to figure out what you can afford in the short term and compare that to what you might pay in the long term. This goes beyond monthly income and expenditures to the heart of your bank accounts.

Wealthier individuals tend to opt for higher deductibles because they have plenty of savings to cover potential damages. Those of us that are a bit less endowed may crave, or even need, lower premiums. An emergency fund is a good account to reference while you’re running the numbers and trying to figure out whether you should aim high or low when it comes to your deductible. As long as you have enough savings to cover at least six months of expenses, you can probably shell out more than the standard $500 deductible.

How risk averse are you?

Deductibles are about more than just your finances, though. Picking your deductible amount is a lot like gambling. You’re hedging your bets, deciding how risk is shared between you and your insurance provider. Insurance is meant to be a safety net that your family can rely on when there’s an unforeseen event. Whether it’s lender-required insurance or not, a policy can help homeowners start over if something bad happens. Most of us would be at a total loss without it.

Yet for some of us, taking on more risk in exchange for lower premiums is worth it. Redistributing some of your home’s risk to yourself lets your provider reduce your premiums. For others, assuming more risk would be too financially and physically stressful.

How likely are you to file a claim?

When it comes to our homes, some of us are into DIY while others would rather hire someone to take care of certain tasks. If you’re a member of the latter group, you’re probably more likely to file a claim when something goes awry. Keep in mind that your claims record is an important factor in determining policy costs. The more claims you file, the higher your premiums will be.

While deciding whether to go with a low or high deductible, you should also consider how likely you’ll need an insurance payout. After all, you’ll only have to pay a deductible when you’re filing a claim. According to the Insurance Information Institute, about one in 15 insured homes has a claim each year and the average person files a homeowners insurance claim only once every eight to ten years.

Here’s something else to consider: Just because you file a claim doesn’t mean it’s going to get approved. A home insurance policy in particular won’t cover everything in your house that needs to be repaired or replaced.

You’ll need to think twice about where your home is located as well. Certain places are more dangerous than others. Homeowners in coastal areas may be more vulnerable to flooding while those in the Great Plains are more likely to experience tornadoes. There are different deductible rules associated with different disasters. If your home is in a high-risk area, you should think long and hard about how much you’ll be able to fork over if disaster strikes.

Bottom line

The internal deductible debate is all about identifying the highest amount you can easily afford and feel comfortable with. If you choose to raise your deductible, you may want to think about adding an endorsement or rider to your policy. That way, you can protect any valuables that may fall outside of the scope of a standard policy.